"You will can get notification in to your G mail ,when we are upload our new article . so you can follow this blog site. you can see "blank line" on the top line of the blog page, type your gmail and then submit. "

Introduction to Bank Reconciliation

In accounting, a company's cash includes the money in its checking account(s). To safeguard this critical and tempting asset, a company should establish internal controls over its cash. These controls include separating the accounting duties of its employees, depositing all receipts into the company's checking account, paying all bills through the checking account, and having an independent person routinely prepare a bank reconciliation (bank rec, bank statement reconciliation), and more.

The purpose of the bank reconciliation is to be certain that the company's general ledger Cash account is complete and accurate. With the true cash balance reported in the Cash account, the company could prevent overdrawing its checking account or reporting the incorrect amount of cash on its balance sheet. The bank reconciliation also provides a way to detect potential errors in the bank's records.

The bank reconciliation process requires some tedious tasks. For example,

Every check amount on the bank statement must be compared to the check amounts in the company's general ledger Cash account. Any differences, such as the company's outstanding cheque and errors, will become part of the adjustments listed on the bank reconciliation.

Every deposit on the bank statement must be compared to the receipts recorded in the company's Cash account. Any differences, such as a deposit in transit and/or errors, will become part of the adjustments listed on the bank reconciliation.

Other items on the bank statement must be compared to the other items in the company's Cash account. Any differences, such as bank fees, checks returned because of insufficient funds, collections made by the bank, etc., will be part of the adjustments listed on the bank reconciliation.

The adjustments based on the above differences will be added or subtracted from one of the following amounts:

- The unadjusted balance from the bank statement (or online banking information)

- The unadjusted balance from the company's general ledger Cash account

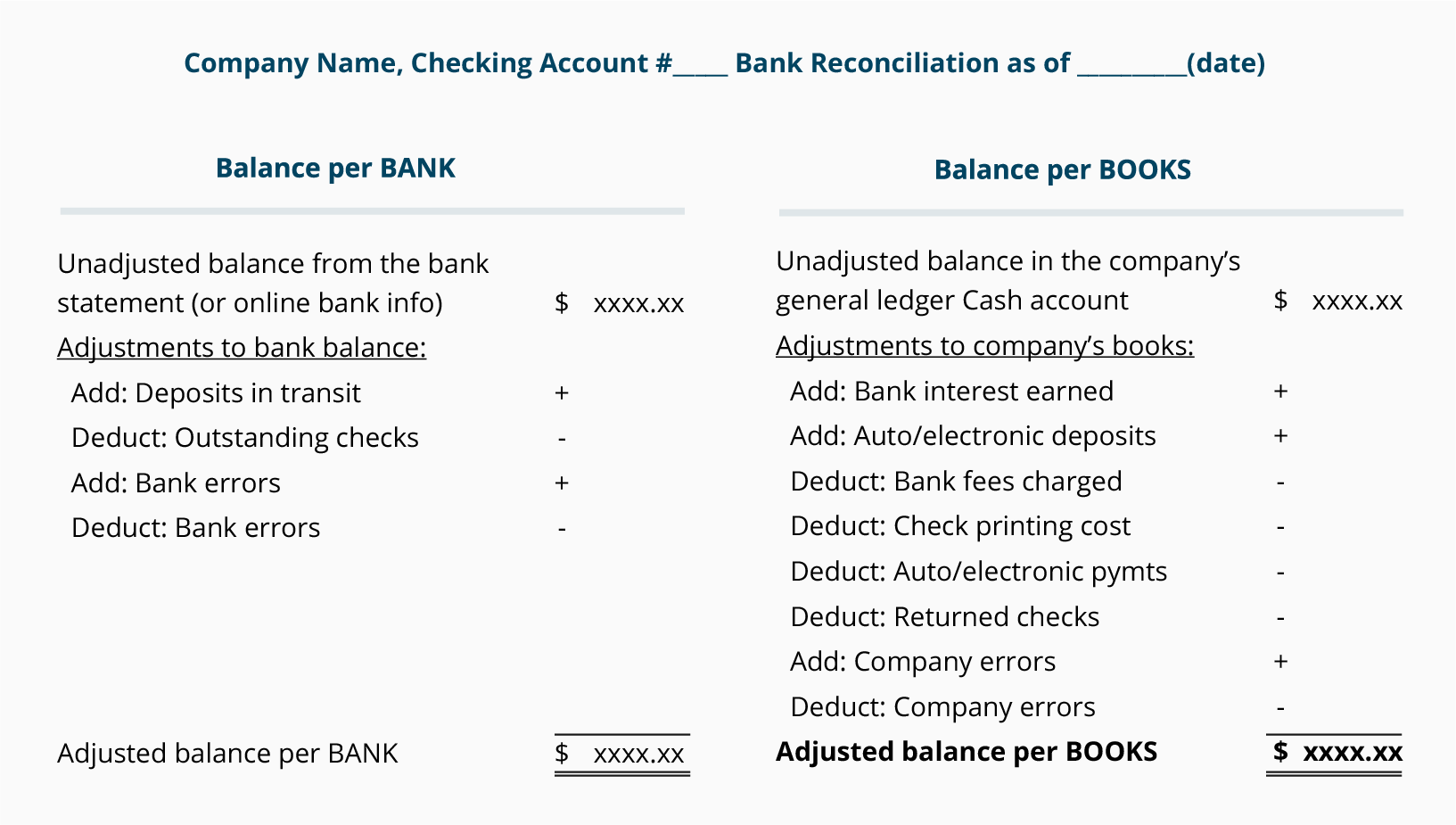

A condensed version of our format for the bank reconciliation is shown here:

Notice the following items in the condensed bank reconciliation format:

The left side is labeled Balance per BANK

The right side is labeled Balance per BOOKS

Adjustments to BANK (shown on the left side) are likely the items that are in the company's general ledger Cash account, but they are not yet recorded in the bank's records. Examples are outstanding checks and a deposit in transit. TIP: Put the item where it isn't.

Adjustments to BOOKS (shown on the right side) are likely the items that the bank has recorded but the items are not yet recorded in the company's general ledger Cash account. Examples include bank fees and a bank credit memo. TIP: Put the item where it isn't.

If the amounts on the bottom line of the bank reconciliation are identical (Adjusted balance per Bank = Adjusted balance per BOOKS), the bank statement is reconciled.

In order for the adjusted balance (which is the true cash balance) to appear in the company's general ledger Cash account and reported on the company's balance sheet, the items listed under Adjustments to BOOKS must be recorded in the company's general ledger accounts.

In the , it was common for a company to prepare the bank reconciliation after receiving the monthly bank statement and before issuing the company's balance sheets. However, with today's online banking a company can prepare a bank reconciliation throughout the month (as well as at the end of the month). This allows the company to verify its checking account balance more frequently and to make any necessary corrections much sooner.

Accounting for Cash at the Company

It is helpful for a company to have a separate general ledger Cash account for each of its checking accounts. For instance, a company will have one Cash account for its main checking account, a second Cash account for its payroll checking account, and so on. For simplicity, our examples and discussion assume that the company has only one checking account with one general ledger account entitled Cash.

As you know, the balances in asset accounts are increased with a debit entry. Therefore, when a company receives money (currency, checks), the company debits its general ledger asset account Cash and credits another account using the date that the money was received (not the date the money is deposited at its bank). For example, if a company receives $900 on Saturday, June 29, the debit to the Cash account (and the credit to another account) will show the date of June 29, even if the money is deposited in the bank account on Tuesday, July 2.

When a company writes a check, the company's general ledger Cash account is credited (and another account is debited) using the date of the check. Therefore, a check dated June 29 will be recorded in the company's accounts using the date of June 29, even if the check clears (is paid through) the company's bank account one week later.

The above transactions are common occurrences that illustrate two important points:

The unadjusted balance in the above company's general ledger Cash account on June 30 is likely to be different from the bank statement balance on June 30.

Often, neither the June 30 unadjusted balance in the company's Cash account nor the June 30 unadjusted balance on the bank statement is the true amount of the company's cash. In that case, both unadjusted balances will need adjustments to arrive at the true, corrected, adjusted cash balance.

Next, we look at how a bank uses debit and credit when referring to a company's checking account transactions.

Accounting at the Bank

To appreciate a bank's use of the terms debit, debit memo, credit, and credit memo, let's take a brief look at a few of the bank's assets and liabilities:

- The bank's assets include cash, investment securities, and loans receivable

- The bank's largest liability is customers' deposits

- Customers' deposits consist of its customers' checking accounts, savings accounts, and certificates of deposit

- Since customers' accounts are liabilities of the bank, they will have credit balances

When a bank customer deposits $900 in its bank checking account, the bank's asset Cash is increased with a debit entry, and the bank's liability Customers' Deposits is increased with a credit entry. The bank's liability has increased because the bank has the liability/obligation to return the customer's checking account balance to the customer on demand

When the bank increases a customer's/depositor's checking account balance, the banker might say that the depositor's checking account was credited. (The credit entry does indeed increase both the depositor's checking account balance and the bank's liability.)

When the bank debits a depositor's checking account, the depositor's checking account balance and the bank's liability to the customer/depositor are decreased.

Here are two examples to reinforce the bank's use of debit and credit with regards to its customers' checking accounts.

Bank Example 1.

Assume that a new company opens a checking account at Community Bank with a deposit of $10,000. Community Bank records the deposit in the bank's general ledger as follows:

- Debit of $10,000 to the bank's asset account Cash

- Credit of $10,000 to the bank's liability account Customers' Deposits

Note that Community Bank credits its liability account Customers' Deposits (which includes the individual depositor's checking account balance). As a result, Community Bank's balance sheet will report an additional $10,000 in assets and an additional $10,000 in liabilities.

Bank Example 2.

Assume that a company pays its August rent of $1,000 by writing a check on August 1. Three days later, the landlord cashes the check at Community Bank. While the company had recorded the $1,000 check in its general ledger accounts with the date of August 1, Community Bank's transaction occurs on August 4. Therefore, using the date of August 4, the bank will record this entry in the bank's general ledger:

- Debit of $1,000 to the bank's liability account Customers' Deposits

- Credit of $1,000 to the bank's asset account Cash

This transaction results in the bank's assets decreasing by $1,000 and its liabilities decreasing by $1,000.

Comparing Accounting: Bank vs. Company

Bank Example 1 showed that the bank credits the depositor's checking account to increase the depositor's checking account balance (since this is part of the bank's liability Customers' Deposits).

However, the depositor/customer/company debits its Cash account to increase its checking account balance.

Bank Example 2 showed that the bank debits the depositor's checking account to decrease the checking account balance (since this is part of the bank's liability Customers' Deposits).

However, the depositor/customer/company credits its Cash account to decrease its checking account balance.

Checking Account Terminology

In this section we provide brief definitions of the terms commonly used when discussing checking accounts and bank reconciliations. We grouped the terms into the following categories:

- General terms for checking accounts

- Terms for adjustments to the balance per bank

- Terms for adjustments to the balance per books

General Terms for Checking Accounts

Checking accounts are known as demand deposit accounts since the bank must pay/return the depositors' account balances (except for uncollected funds) on demand. Companies report the checking account balances as part of its cash. Companies should safeguard their checking accounts through internal controls, which includes timely bank reconciliations prepared by an independent person.

Cheques are a company's written orders to its bank to pay an amount from the company's checking account. Hence, checks state "Pay to the order of ______". The person or company named on the check is known as the payee. The payee is required to endorse (sign the back of) the check as evidence that the money was received. (In place of the endorsement, a bank can indicate that the amount was deposited/credited to the payee's bank account.)

Cancelled checks are the checks the company issued and were paid by the company's bank. Cancelled checks are also referred to as checks that "cleared" the bank account on which they are drawn.

Voided checks are checks that were written in error. These checks will have the word "VOID" clearly written across the front of the check.

Stop payment order is a company's instruction to its bank to not pay a specific check that the company had already written but was not yet paid by the bank. Generally, the bank charges a fee for the special effort required by the customer's order.

Deposits often consist of currency and checks (received from customers) that a company takes to its bank with instructions to add the amount to the company's checking account. The bank records the deposit with the date the bank processes the deposit. (However, the company's general ledger Cash account shows the date that the company had received the money from its customers or others.)

Authorized signers are a limited number of people designated to sign checks drawn on the company's checking account. Their names and signatures appear on a bank signature card along with the approval of the company's key officers.

Bank overdraft occurs when checks written by a company are presented to its bank for payment and the company's checking account balance is not sufficient to pay the checks. If the checks were to be paid, the checking account balance would become a negative amount. Without a prior arrangement with the bank (such as an automatic loan), the bank will likely return or "bounce" the check back to the endorser. (The related terms NSF check and return item are described under Terms for Adjustments to the Balance per Books.)

Uncollected funds occur when a company deposits a check into its bank account, but the check is drawn on an account at a different bank. Since the company's bank is not certain that the check will be honored by the bank on which it is drawn, the company's bank will not allow the company/depositor to use the amount until the deposited check is paid by the other bank. (Some people refer to the amount of outstanding checks as the company's float.)

Terms for Adjustments to the Balance per Bank

Outstanding cheques are checks that a company had written and recorded in its Cash account, but the checks have not yet been paid by the company's bank (or have not "cleared" the bank). It is common for a few checks written in earlier months to remain outstanding at the end of the current month.

Since the outstanding checks are not yet in the bank's records/bank statement, the company's bank reconciliation will show the outstanding checks as a subtraction from the balance per bank.

Deposits in transit are the cash and checks a company has received and recorded in its general ledger accounts, but the cash and checks have not been processed by the bank as of the date of the bank reconciliation. Deposits in transit are sometimes referred to as outstanding deposits.

Since the deposits in transit are not yet recorded in the bank's records, the company's bank reconciliation will show the deposits in transit as an addition to the balance per bank.

Bank errors are mistakes made by the bank that were discovered when the company prepared the bank reconciliation. While these items are rare, they do occur. For example, if a company issues a check for $867, but the bank paid the check at the incorrect amount of $876, there is a $9 bank error. This bank error will be shown on the company's bank reconciliation as an addition of $9 to the unadjusted balance per bank (since the bank had reduced the bank account by $9 too much).

The company should immediately contact the bank so the bank can make the correction to the company's checking account balance. (There is no entry made by the company since the company's general ledger Cash account already contains the correct amount of $867.)

Terms for Adjustments to the Balance per Books

Bank credit memos indicate that the bank increased the balance in a company's checking account. For example, if a bank lends $50,000 to a company, the bank is likely to deposit the loan proceeds in the company's checking account by means of a credit memo.

A bank credit memo is recorded in the bank's general ledger with a credit to the bank's liability account Customers' Deposits (causing this liability's account balance to increase). The bank also debits its asset account Loans Receivable (causing this asset's balance to increase).

If the bank's credit memo was not recorded in the company's general ledger accounts as of the date of the bank reconciliation, the company lists the credit memo amount as an adjustment to increase the balance per books. This adjustment must also be recorded in the company's general ledger with a debit to Cash and a credit to Loans Payable or Notes Payable.

Bank debit memos indicate that the bank has decreased the balance in a company's checking account. Examples include bank fees (service charge, overdraft fee, stop payment fee, etc.) and loan payments.

A bank debit memo is recorded in the bank's general ledger with a debit to the bank's liability account Customers' Deposits (and a credit to another account).

If the amount of the debit memo was not recorded in the company's general ledger accounts as of the date of the bank reconciliation, the company lists the debit memo amount as a decrease to the balance per books. This adjustment must also be recorded in the company's general ledger with a credit to Cash and a debit to Bank Fees Expense.

ACH, EFT, Zelle transfers, and wire transfers can indicate additions to or subtractions from a company's bank account without the company preparing a deposit slip or writing a cheque. ACH is the acronym for Automated Clearing House. EFT is the acronym for Electronic Funds Transfer.

If any of these transfers were not recorded in the company's general ledger as of the date of the bank reconciliation, the company will list them on the bank reconciliation as adjustments to the balance per books. The company must record these transfers in its general ledger accounts.

NSF cheque is a check issued by a company, but the bank did not pay/honor the check because the company's bank balance was less than the amount of the check. Unless the company had arranged for this situation, the company's bank is likely to return the check to the endorser (instead of allowing the checking account to have a negative balance.) When the bank returns the NSF check, the check will be noted as Not Sufficient Funds (NSF) or Insufficient funds. An NSF check is also known as a check that "bounced" or as a "rubber check" (since the check is being bounced back by the bank).

Return item is typically a check that was not paid/honored by the bank on which it was drawn. A few examples include an NSF check, a check drawn on a checking account that was closed, and a check where the maker of the check has stopped payment.

Company errors may require additions or subtractions from the company's general ledger Cash account. One type of error is a transposition error which involves the switching of digits within an amount. For example, the amount $789 might be incorrectly recorded as $798, resulting in a difference of $9. Perhaps $1,458 was recorded as $1,548, resulting in a difference of $90. Another type of error involves omitting or adding a zero, such as recording $500 instead of the actual amount of $5,000 (a difference of $4,500).

In these types of errors, the differences are evenly divisible by 9: $9/9 = 1; $90/9 = 10; $4,500/9 = 500. If your bank reconciliation does not balance and the difference is evenly divisible by 9, you may be able to rule out many amounts in your effort to identify the error.

Company's Process for Preparing its Bank Reconciliation

The process for preparing the bank reconciliation of a company's checking account includes:

Identifying and reviewing any difference between every amount on the bank statement (or the online banking information) and every amount in the company's Cash account.

Determining the true/correct/adjusted balance for the company's Cash. This is done by listing the unadjusted balance from the bank statement, the unadjusted balance from the company's Cash account, and then listing the adjustments (differences) that were identified.

Recording the pertinent adjustments to the company's Cash account.

We suggest the following five steps for preparing a bank reconciliation:

Step 1. Compare every amount on the bank statement (or in the bank's online information) with every amount in the company's general ledger Cash account and note any differences.

Compare the amount of every check that was paid by the bank (cleared the bank account) with the amount of every check in the company's Cash account. Any differences, such as the outstanding checks and errors, must be shown on the bank reconciliation.

Compare every deposit processed by the bank with the receipts recorded in the company's Cash account. Any differences, such as a deposit in transit and/or errors, must be shown on the bank reconciliation.

Compare other items on the bank statement with the other items in the company's Cash account. Any differences, such as bank fees, checks returned because of insufficient funds, collections made by the bank, etc., must be shown on the bank reconciliation.

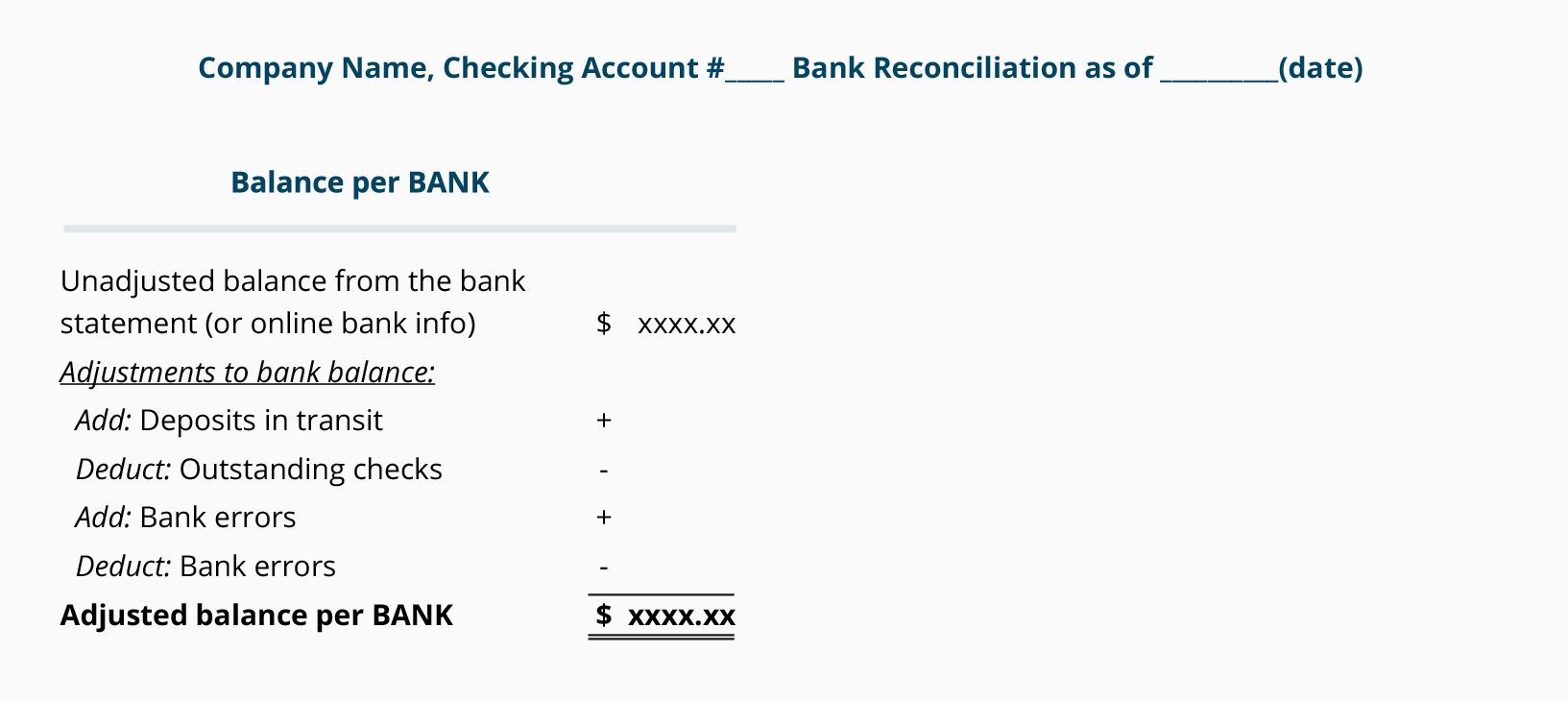

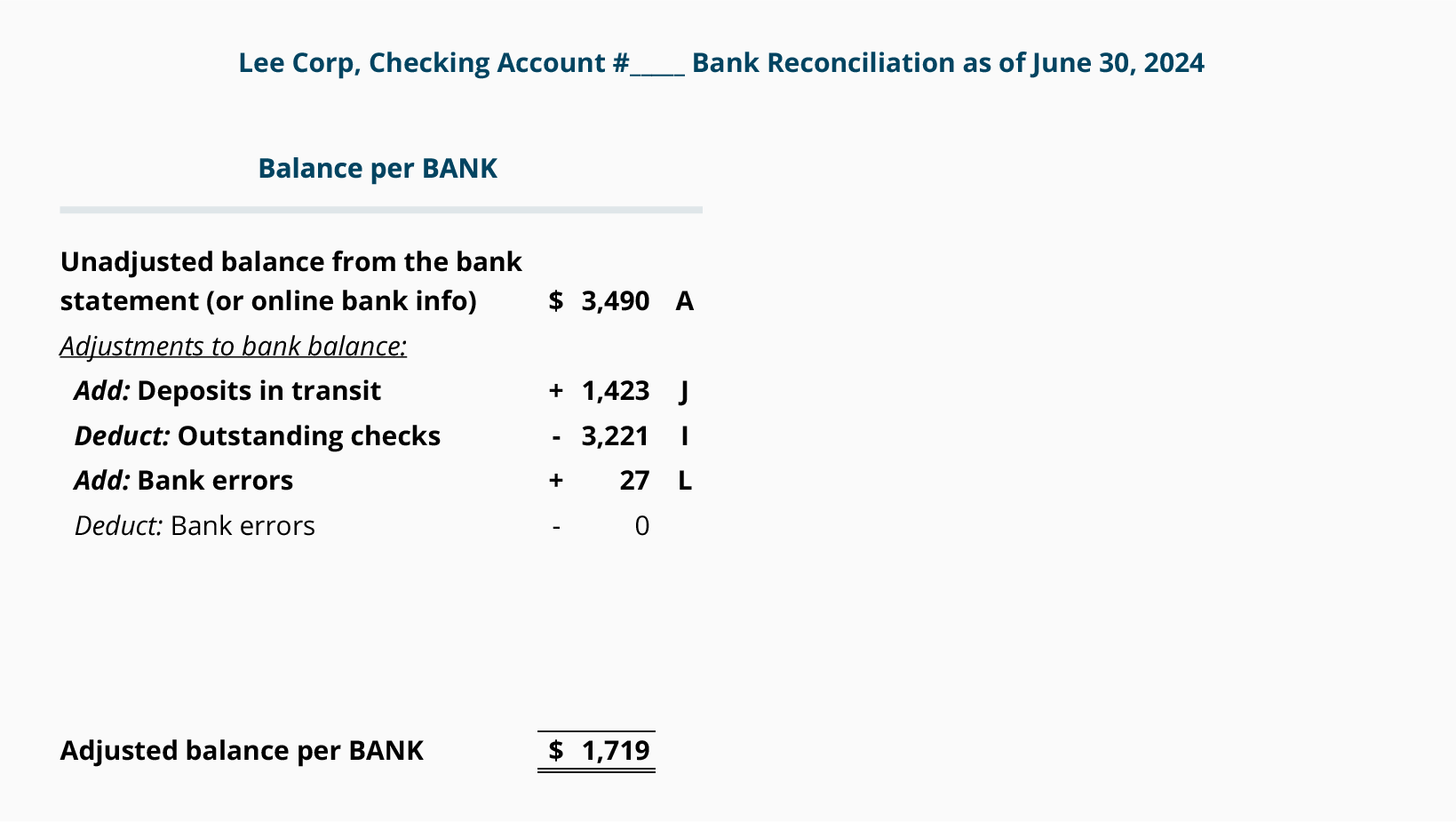

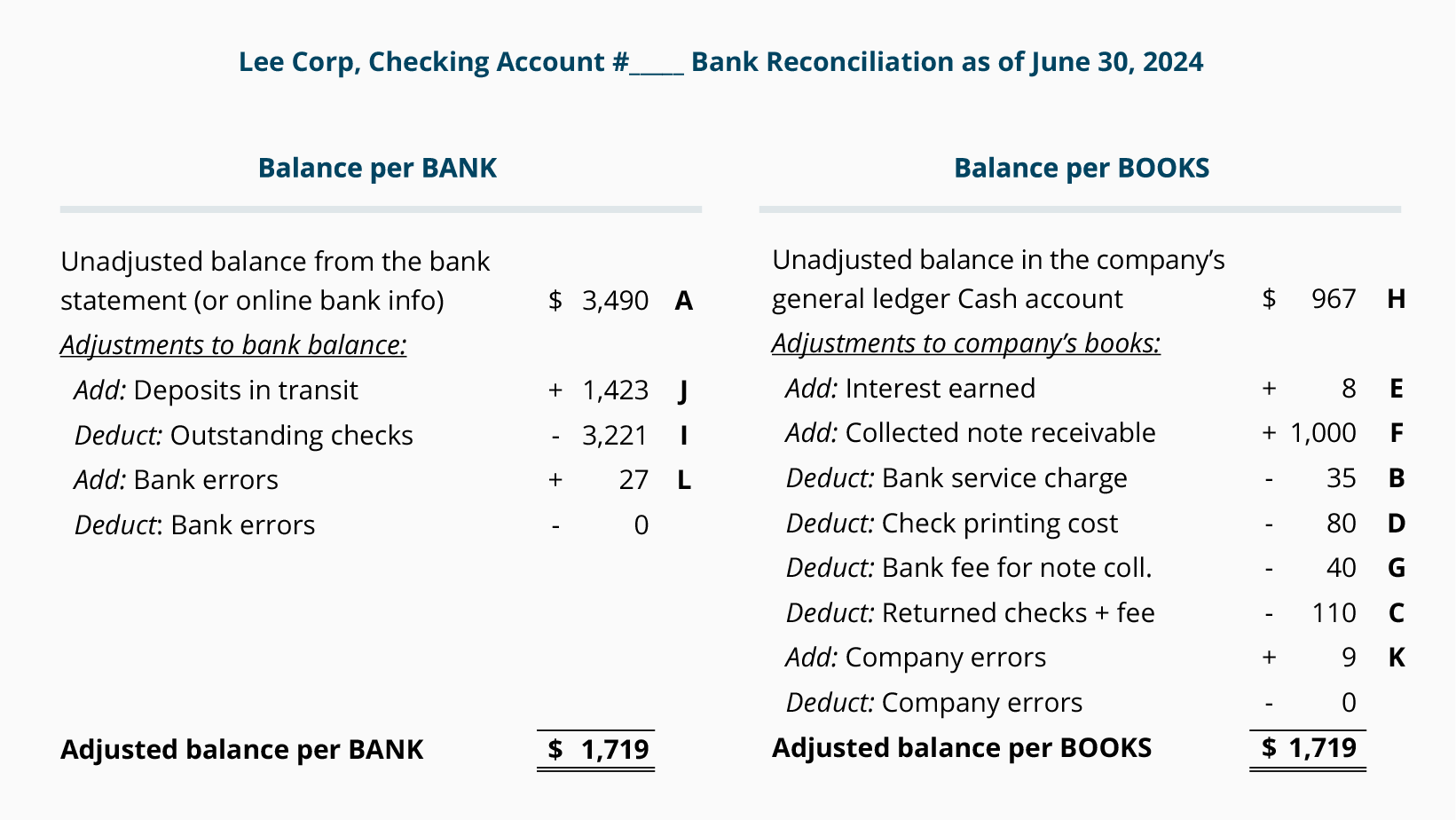

Step 2. Complete the Balance per BANK side of the bank reconciliation format.

The Balance per BANK side of the bank reconciliation requires the following:

Enter the unadjusted balance from the bank statement (or online banking information).

Add any deposits in transit. These are receipts in the company's Cash account that have not been processed by the bank as of the date of the bank reconciliation.

Subtract any outstanding checks. These are the checks the company had issued and recorded in its Cash account, but they have not been paid by the bank (not cleared the bank account) as of the date of the bank reconciliation.

Add/subtract other items with amounts that were incorrectly recorded by the bank.

Combine the above amounts and show the total amount on the bottom line, Adjusted balance per BANK

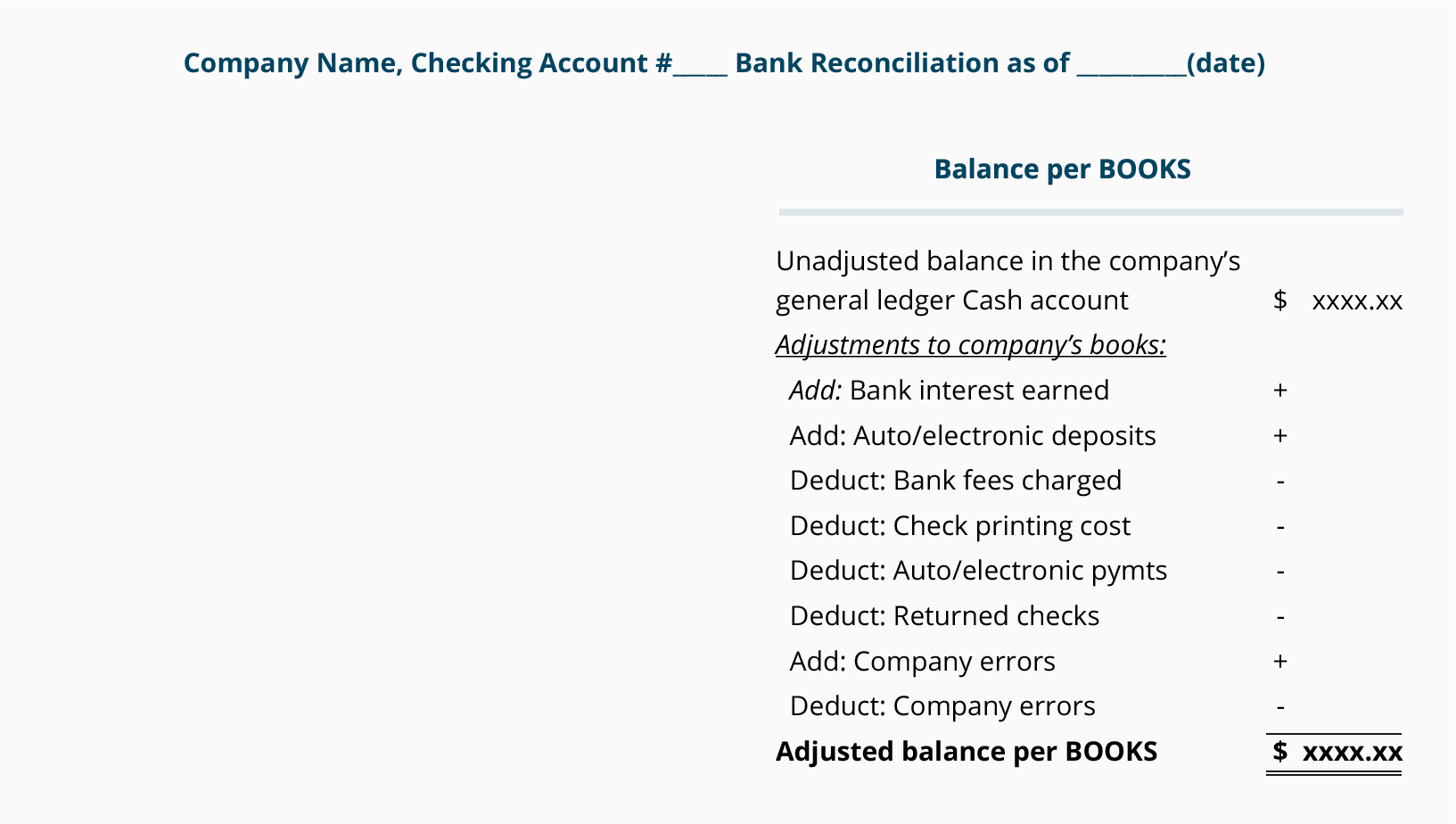

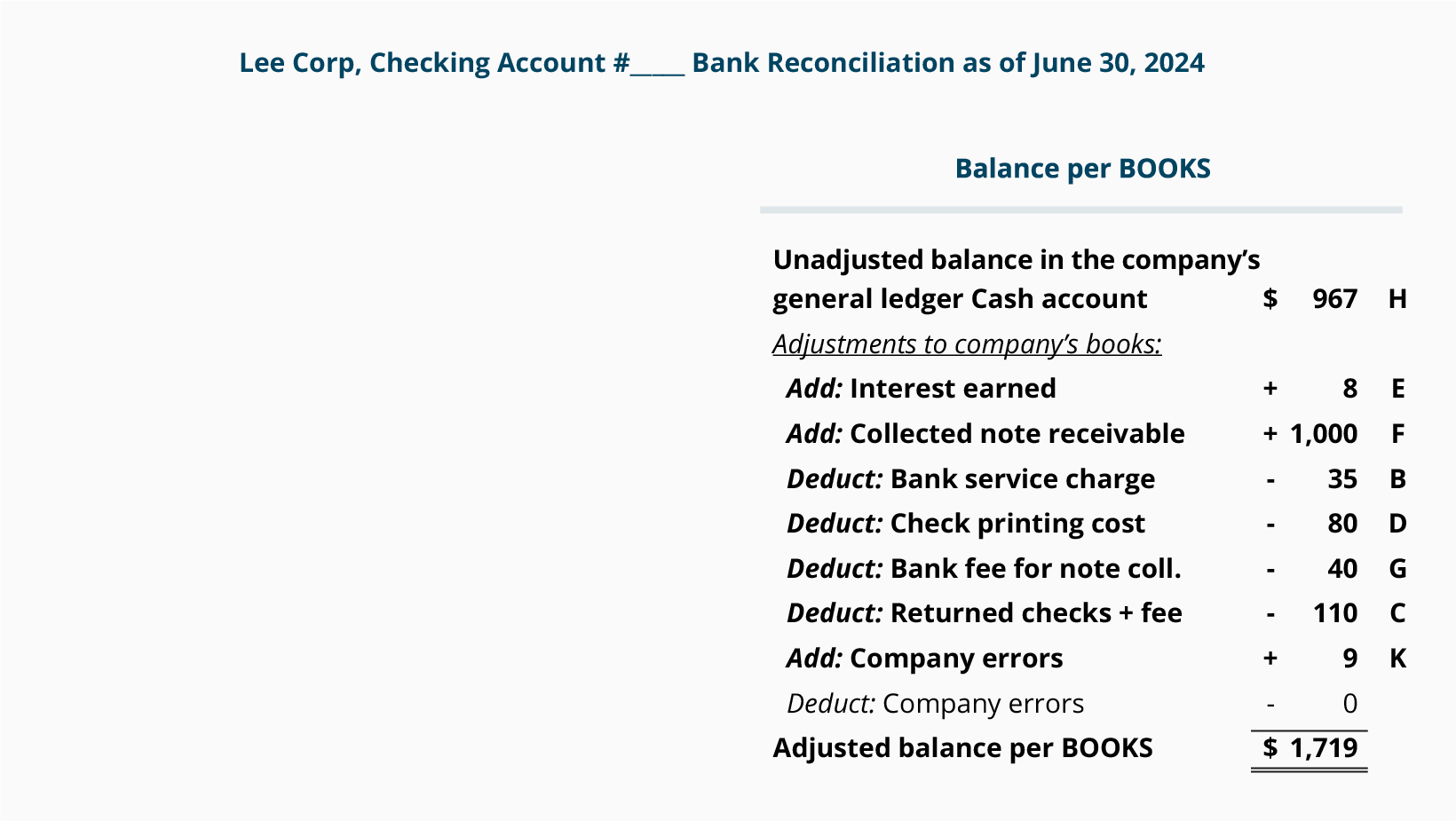

Step 3. Complete the Balance per BOOKS side of the bank reconciliation format.

The Balance per BOOKS side of the bank reconciliation requires the following:

Enter the unadjusted balance appearing in the company's general ledger Cash account.

Add any increases (interest earned, bank credit memos) that are shown on the bank statement but were not yet recorded in the company's Cash account.

Subtract any decreases (such as bank services charges, return items, bank debit memos) that are shown on the bank statement but are not yet recorded in the company's Cash account.

Add/subtract other items with amounts that were incorrectly recorded by the company.

Combine the amounts on the right side and show the total on the bottom line, Adjusted balance per BOOK

Step 4. Be certain that the bank reconciliation shows Adjusted balance per BANK = Adjusted balance per BOOKS.

The bottom line of both sides of the bank reconciliation must be the same amount. In other words, Adjusted balance per BANK must equal Adjusted balance per BOOKS.

Note: Having the Adjusted balance per BANK = Adjusted balance per BOOKS does not guarantee that the company's cash has been completely accounted for. For instance, if an employee had stolen some of the company's cash receipts before the money was recorded in the company's accounts (and obviously not deposited in the company's bank account) the missing amount will not be detected by the bank reconciliation.

Step 5. Record in the company's general ledger the adjustments to the balance per BOOKS.

Since the adjustments to the balance per the BOOKS have not been recorded as of the date of the bank reconciliation, the company must record them in its general ledger accounts.

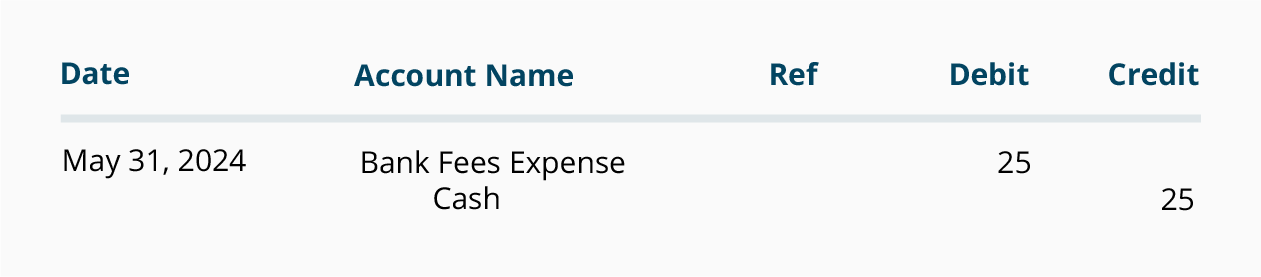

For example, if one of the adjustments to the balance per BOOKS is a $25 service charge (that was on the bank statement on May 31, 2019 but not yet recorded in the company's general ledger), the company must post the following entry:

Note: After recording/posting the adjustments to the general ledger accounts, it is important to confirm that the company's general ledger Cash account balance is indeed equal to the Adjusted balance per BOOKS shown on the bottom line of the bank reconciliation.

Next, we will prepare a bank reconciliation for a hypothetical company by using transactions that are commonly encountered.

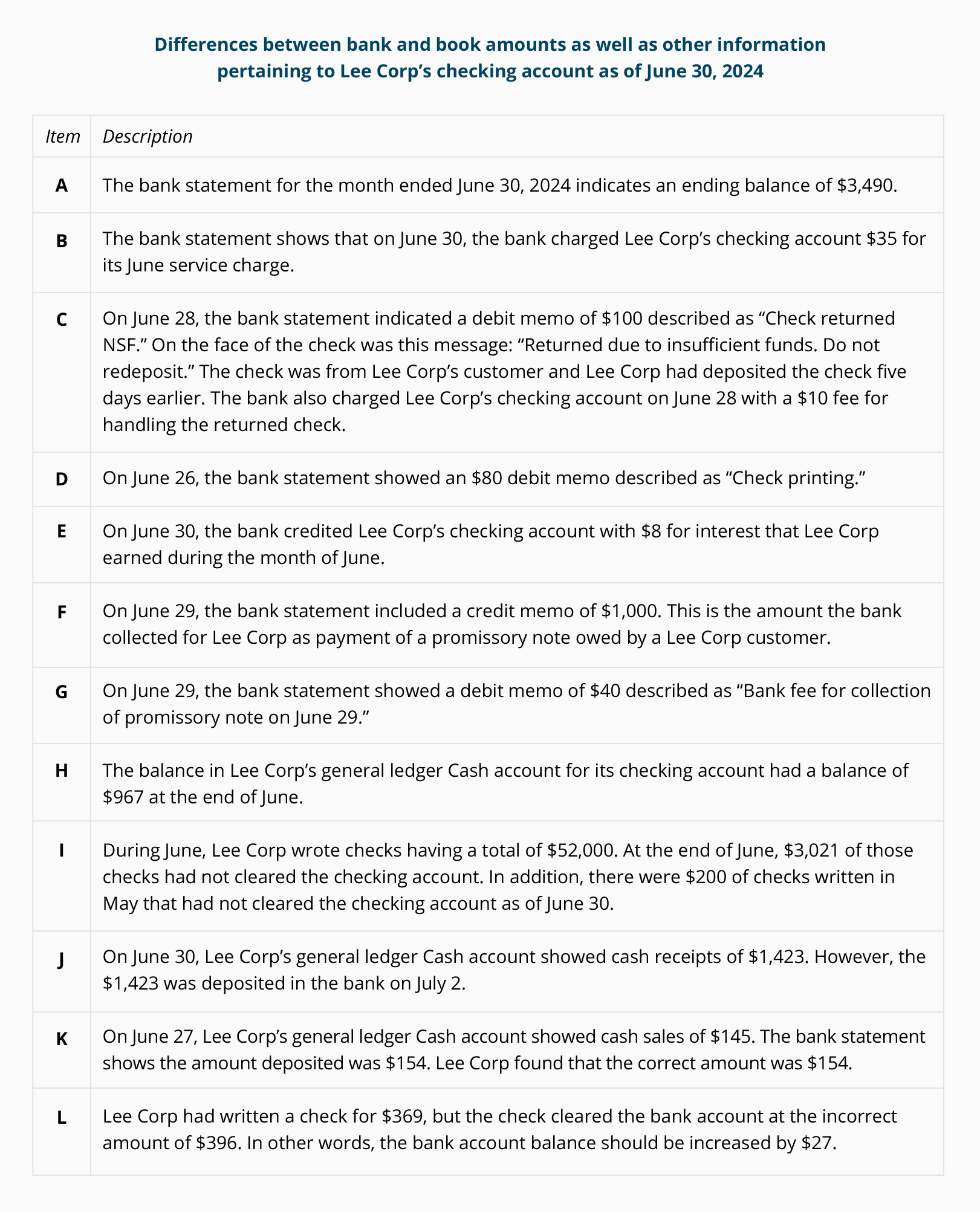

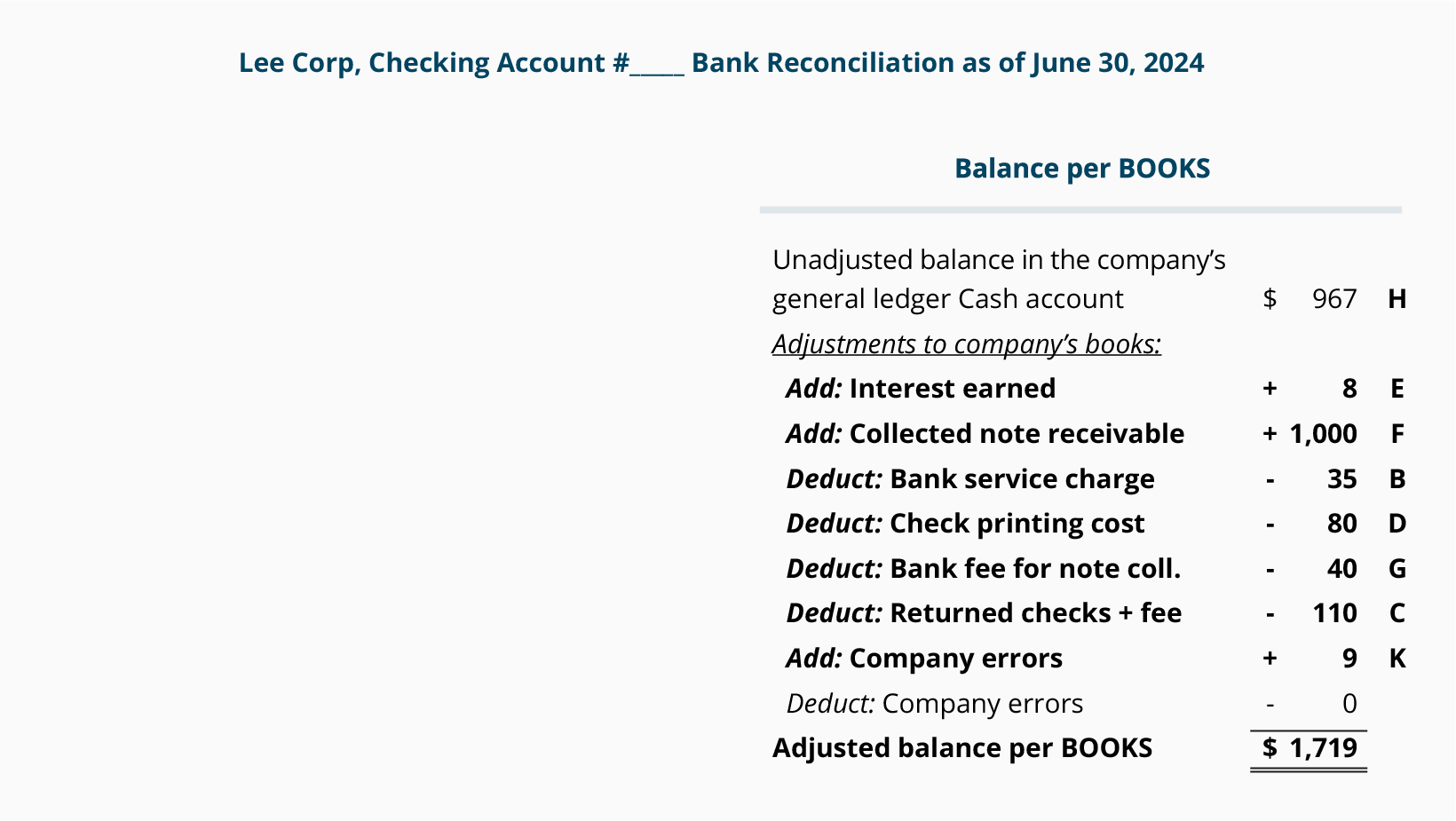

Sample of a Company's Bank Reconciliation with Amounts

In this section we will prepare a June 30 bank reconciliation for Lee Corp using the five steps discussed above.

Step 1. Compare every amount on the bank statement (or the bank's online information) with every amount in the company's general ledger Cash account and note any differences.

After comparing every item on the bank statement (checks paid, deposits processed, other items) with every item in Lee Corp's general ledger Cash account (checks written, money received, other items), we listed the differences and other pertinent information in the table that follows.

(The letter in the "Item" column will be shown on the bank reconciliation next to the amount.)

Keep in mind our TIP: Put the item where it isn't. This means:

If an item appears on the bank statement (but isn't in the company's general ledger), put the item on the bank reconciliation under Adjustments to BOOKS

If an item is already in the company's general ledger Cash account (but it isn't on the bank statement), put the item on the bank reconciliation under Adjustments to BANK

Step 2. Complete the Balance per BANK side of the bank reconciliation format.

Step 3. Complete the Balance per BOOKS side of the bank reconciliation format.

Step 4. Be Certain the Adjusted Balance per BANK = Adjusted Balance per BOOKS.

Since the Adjusted balance per BANK of $1,719 is equal to Adjusted balance per BOOKS of $1,719, the bank statement of August 31 has been reconciled.

Step 5. Record in the company's general ledger the adjustments to the balance per BOOKS.

Recall that the adjustments to the balance per BOOKS will require accounting entries for the items to be posted to the company's general ledger accounts.

For each of the adjustments shown on the Balance per BOOKS side of the bank reconciliation, a journal entry is required. Each journal entry will affect at least two accounts, one of which is the company's general ledger Cash account.

[Note: The company does not make accounting entries for the adjustments to the bank's records.]

The following are the necessary entries for the adjustments to the balance per BOOKS. We reference each entry as E, F, B, D, G, C, or K, as indicated on the right side of the bank reconciliation.

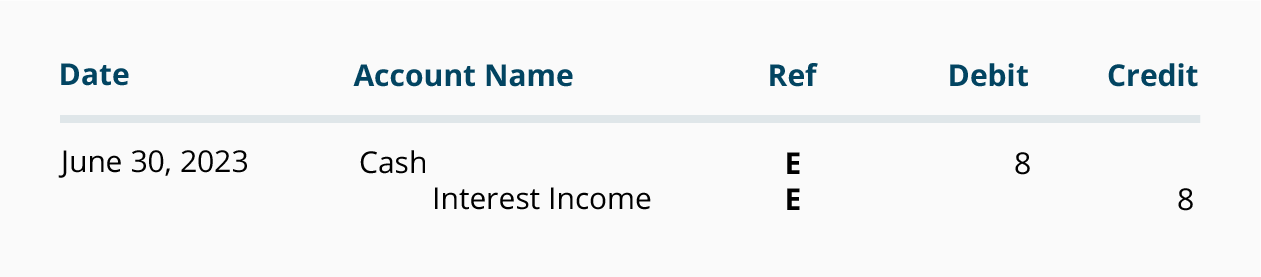

Adjustment E

The bank statement showed that on June 30, the bank added $8 of interest that had been earned by Lee Corp. Assuming that this was not yet recorded in Lee Corp's general ledger, the following journal entry is required:

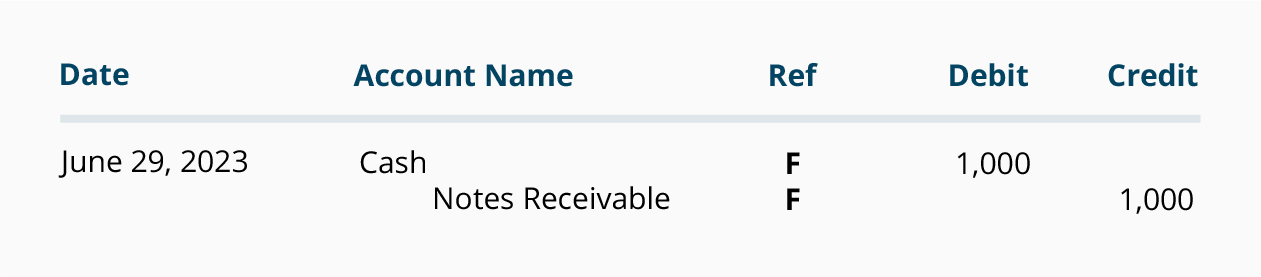

Adjustment F

On June 29, the bank statement showed a bank credit memo of $1,000 which caused the checking account balance to increase. We assume that Lee Corp had not yet recorded the collection of the note in its general ledger accounts. Therefore, Lee Corp must increase its Cash account balance and decrease the balance in its asset account Notes Receivable. This is achieved by the following journal entry:

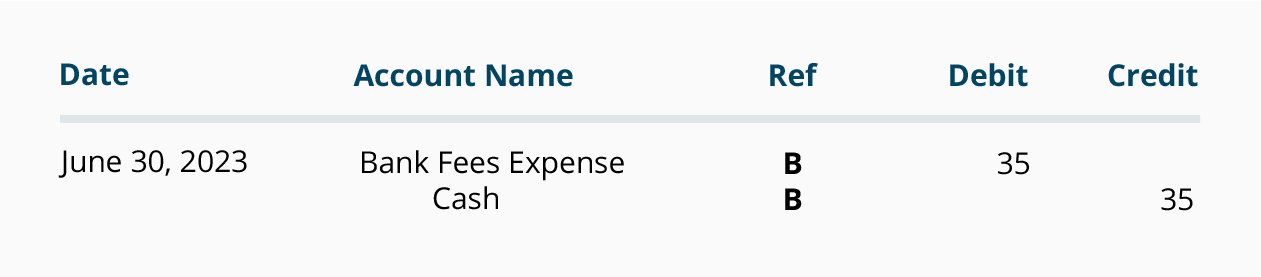

Adjustment B

The bank statement shows a service charge of $35 on June 30. Since this reduced the balance in Lee Corp's checking account, Lee Corp must credit its Cash account and debit an expense such as Bank Fees Expense. Lee Corp's entry is:

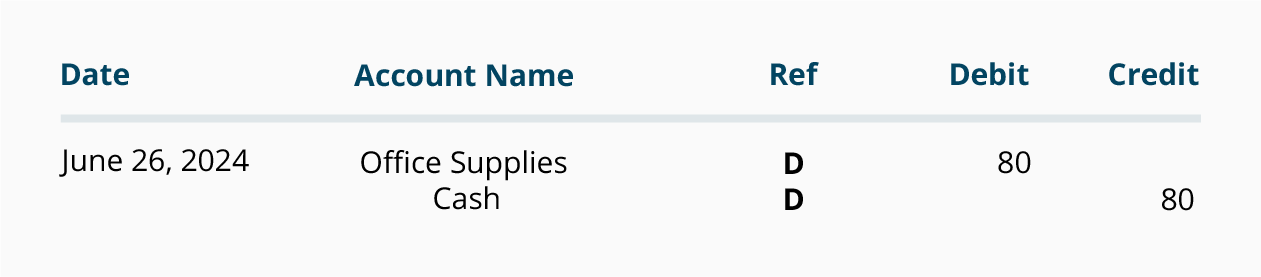

Adjustment D

On June 26, the bank statement showed that the bank processed a debit memo of $80 for the printing of Lee Corp's checks. While the bank debits its liability account Customers' Deposits to reduce its credit balance, Lee Corp must credit its asset account Cash to reduce its debit balance. Assuming that Lee Corp has not yet recorded the $80 printing cost, Lee Corp will record this journal entry:

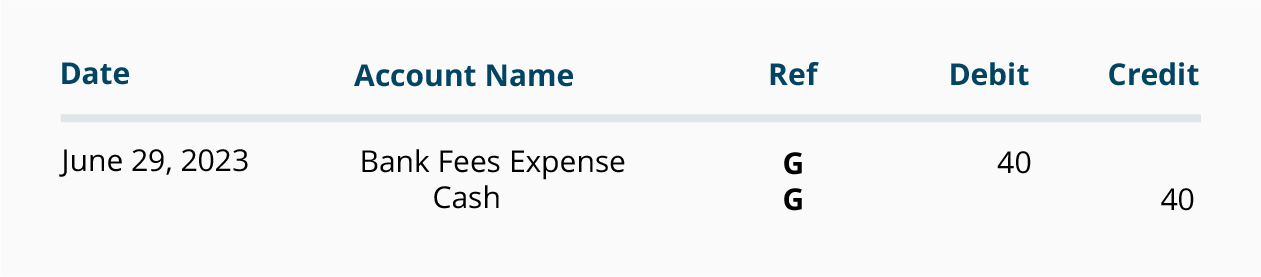

Adjustment G

On June 29, the bank statement showed a debit memo of $40 for the bank's fee for collecting a note receivable for Lee Corp. Since this reduces Lee Corp's checking account balance, Lee Corp will need to reduce the balance in its general ledger asset account Cash. Assuming this has not yet been recorded, the following entry is needed:

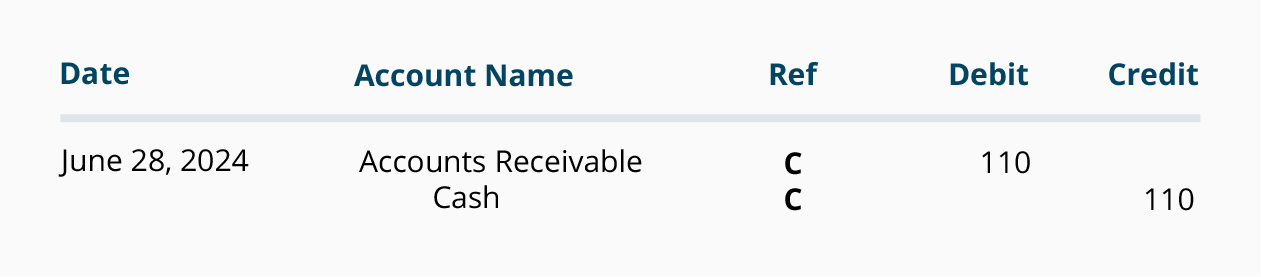

Adjustment C

On June 28, the bank statement showed that Lee Corp's checking account balance was decreased by $110 for a check that Lee Corp had deposited in its checking account. (The deposited check was not paid by the bank on which it was drawn and was returned.) As a result, Lee Corp must reduce its general ledger Cash account by $110. Assuming this was not yet recorded by Lee Corp, it will record the following entry:

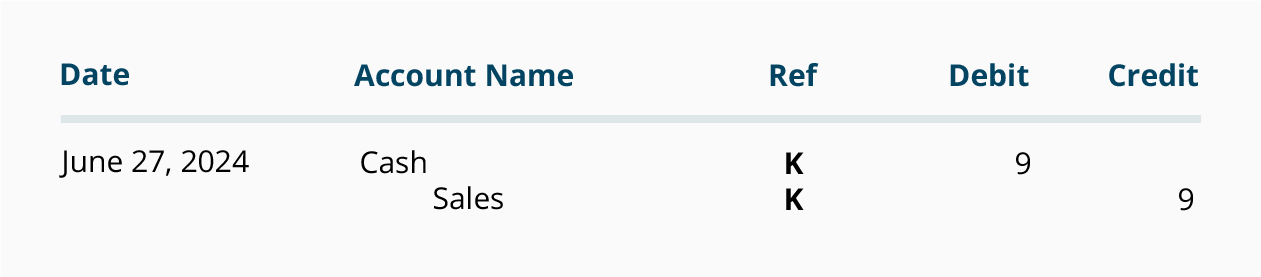

Adjustment K

On June 27 Lee Corp had increased its Cash account and its Sales account by $145. While reconciling its August bank statement, Lee Corp learned that the correct amount was $154. Therefore, Lee Corp must increase its Cash account balance by $9 and increase its Sales by $9. (Instead of removing the $145 and then adding $154, Lee Corp is adding the difference of $9 to the accounts.)

Note: After the above entries are posted to the general ledger accounts, it is important to confirm that the balance in the Cash account is equal to the Adjusted balance per BOOKS shown on the bank reconciliation.

It is also necessary to contact the bank immediately for any bank errors that were discovered in order for the bank account to be corrected.

THANK YOU..

We recommend that you now take our free Practice Quiz for this topic so that you can...

https://www.blogger.com/u/1/blog/post/edit/preview/2917250908721901155/2686214350333642132

- See what you know

- See what you don't know

- Deepen your understanding

- Improve your retention

FOLLOW US.

Presenting by -Accounting way

for more information -

follow "accounting way" official face book account

subscribe and click the bell icon, to "Accounting tutorials" YouTube channel for practicing knowledge

YouTube channel link mentioned below

https://www.youtube.com/channel/UCpe3Z6l310iM4RcZO1-2mlw

No comments:

Post a Comment