"You will can get notification in to your E mail ,when we are upload our new article . so you can follow this blog site. you can see "follow button on the top line of the blog page, click it. "

Audit Process

PART 02

Accounting Equation for a Sole Proprietorship: Transactions 7–8

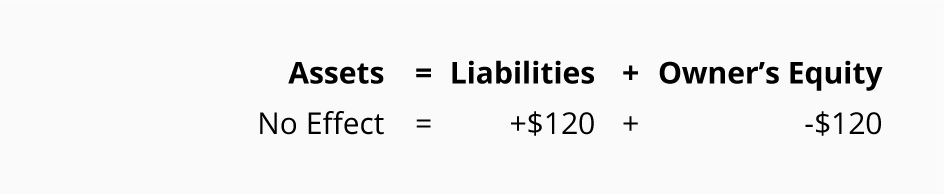

Sole Proprietorship Transaction #7.

On December 7, 2019 ASC uses a temporary help service for 6 hours at a cost of $20 per hour. ASC will pay the invoice when it is due in 10 days. The effect on its accounting equation is:

ASC's liabilities increase by $120 and the expense causes owner's equity to decrease by $120.

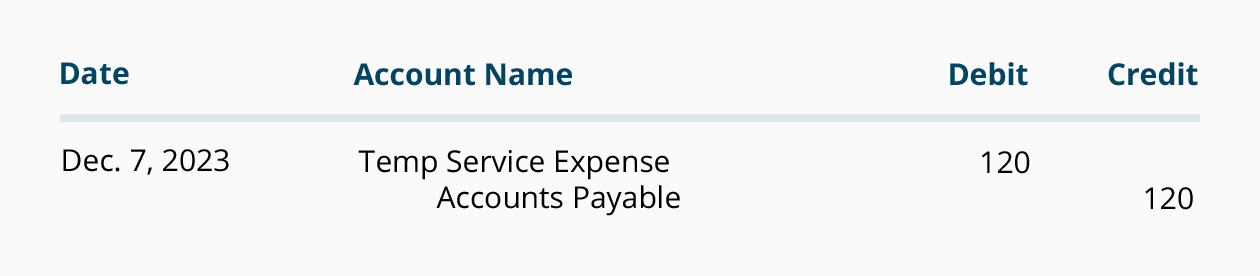

The liability will be recorded in Accounts Payable and the expense will be reported in Temp Service Expense. The journal entry for recording the use of the temp service is:

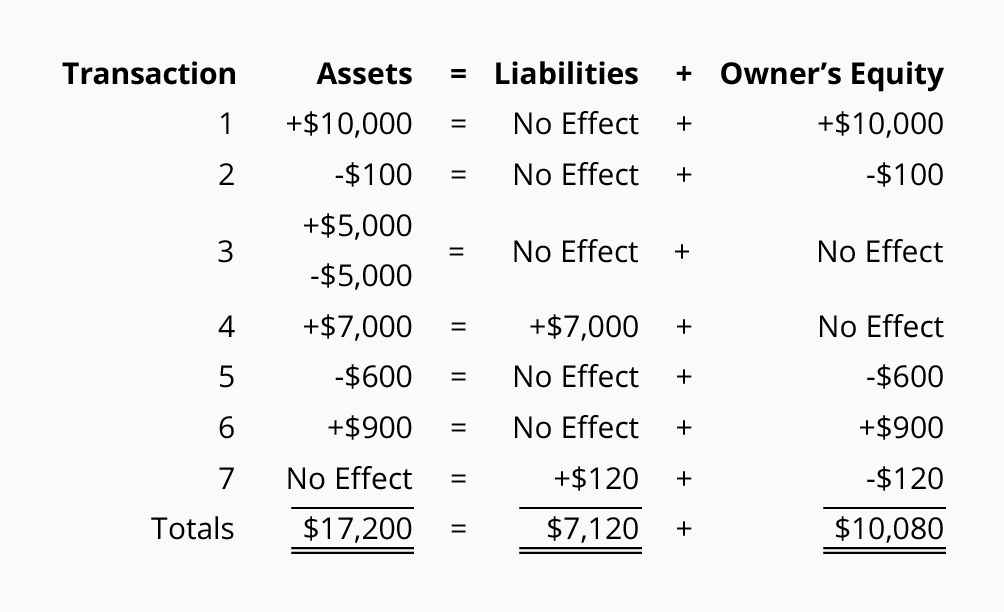

The effect of the first seven transactions on the accounting equation can be viewed here:

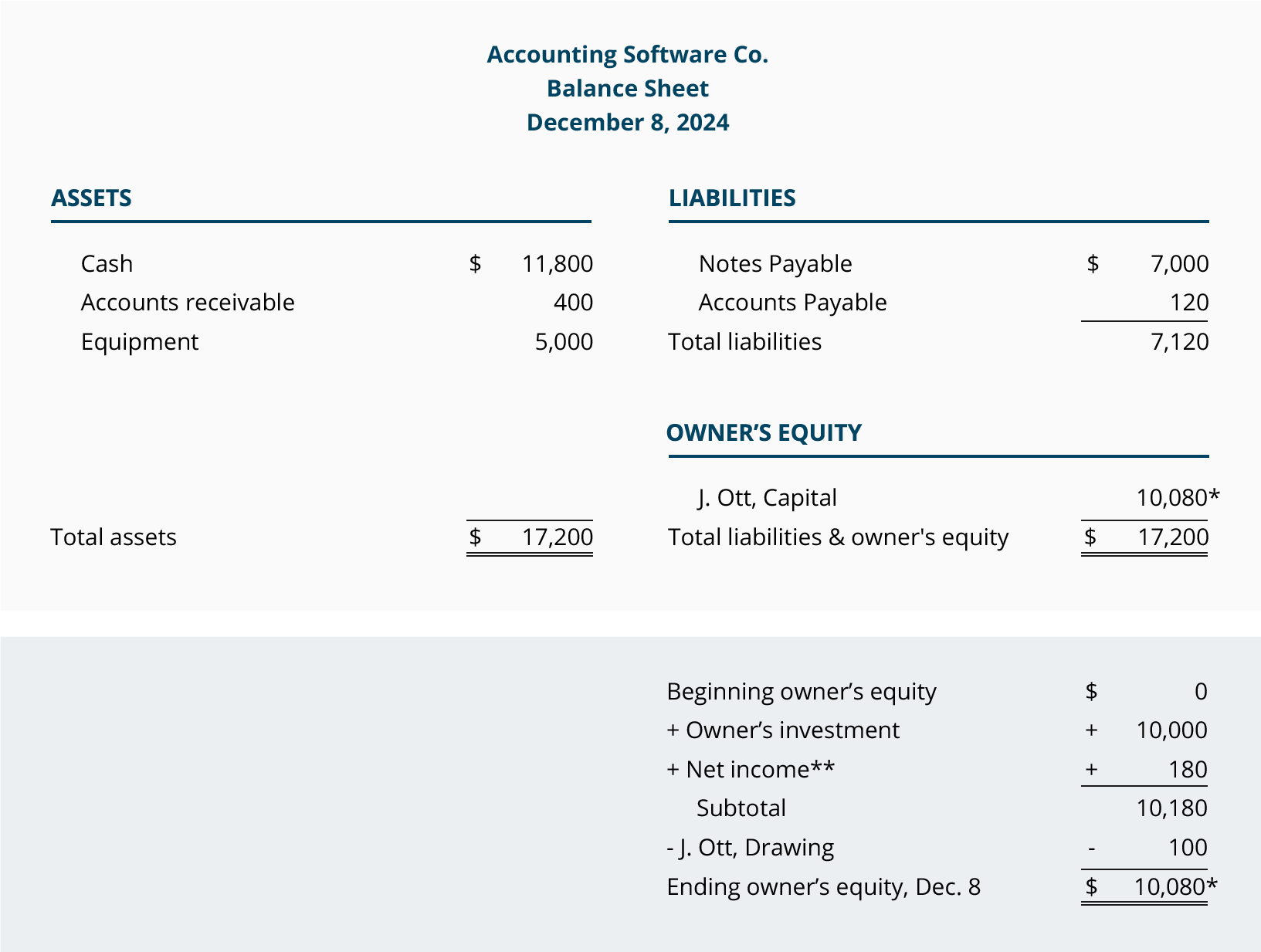

The totals show us that the company has assets of $17,200 and the sources are the creditors with $7,120 and the owner of the company with $10,080. The accounting equation totals also tell us that the company has assets of $17,200 with the creditors having a claim of $7,120. This means that the owner's residual claim is $10,080.

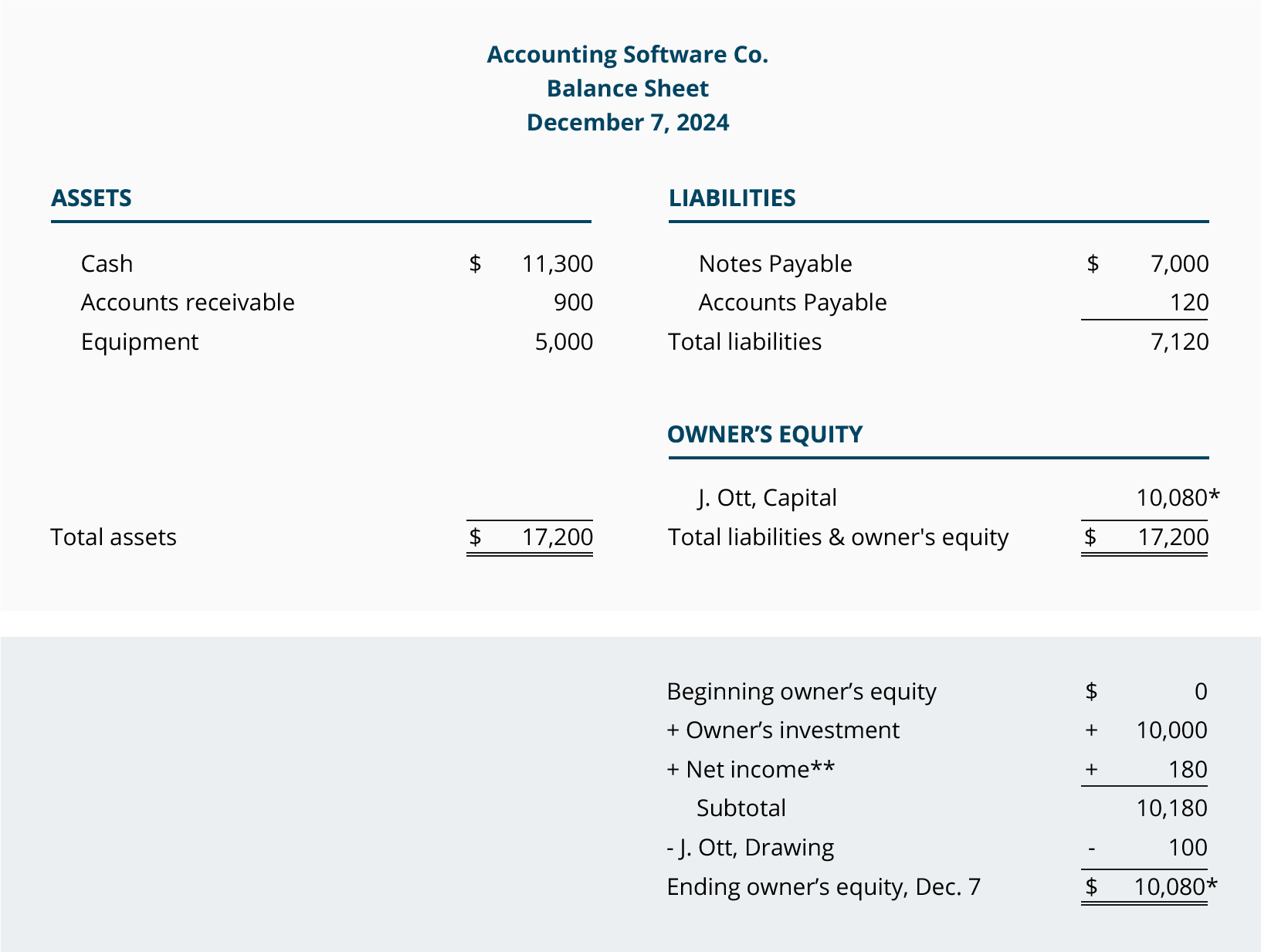

The financial position of ASC as of midnight on December 7, 2019 is:

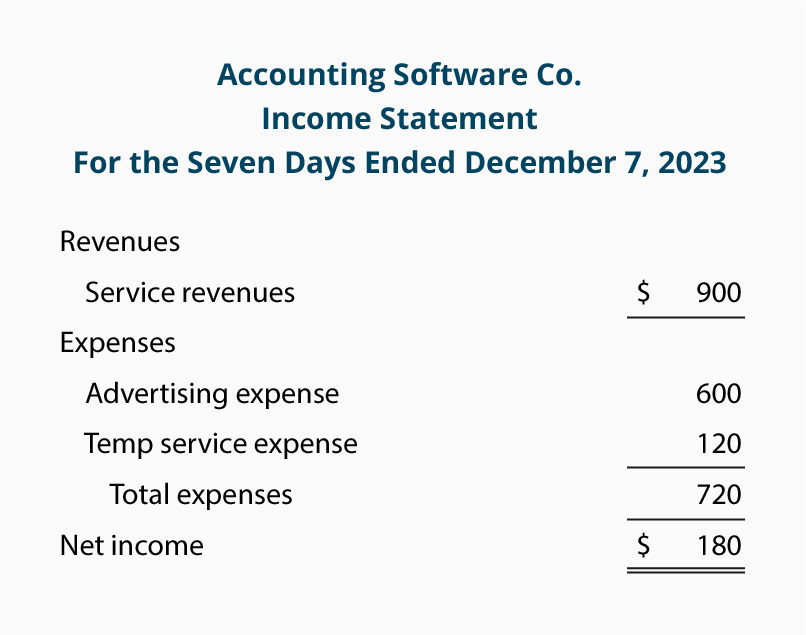

**The income statement (which reports the company's revenues, expenses, gains, and losses for a specified time interval) is a link between balance sheets. It provides the results of operations—an important part of the change in owner's equity.

Accounting Software Co.'s income statement for the first seven days of December is:

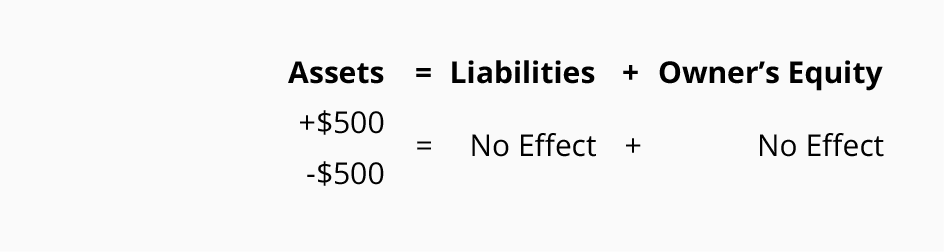

Sole Proprietorship Transaction #8.

On December 8, 2019 ASC receives $500 from the clients it had billed on December 6, 2019. The collection of accounts receivables has this effect on the accounting equation:

The company's asset (cash) increases and another asset (accounts receivable) decreases. Liabilities and owner's equity are unaffected. (There are no revenues on this date. The revenues were recorded when they were earned on December 6.)

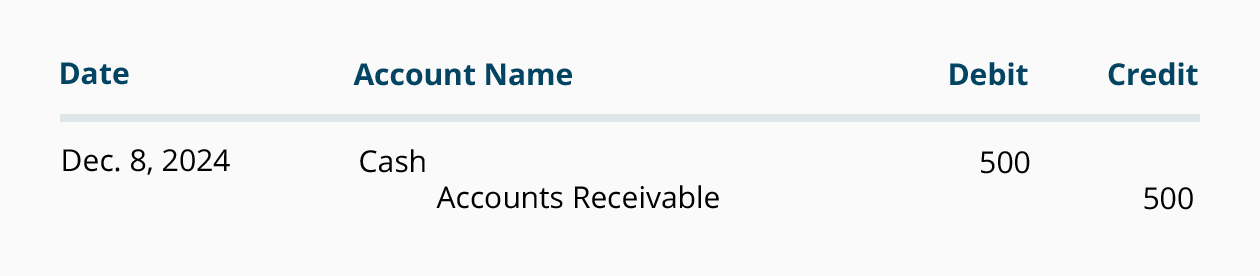

The general journal entry to record the increase in Cash, and the decrease in Accounts Receivable is:

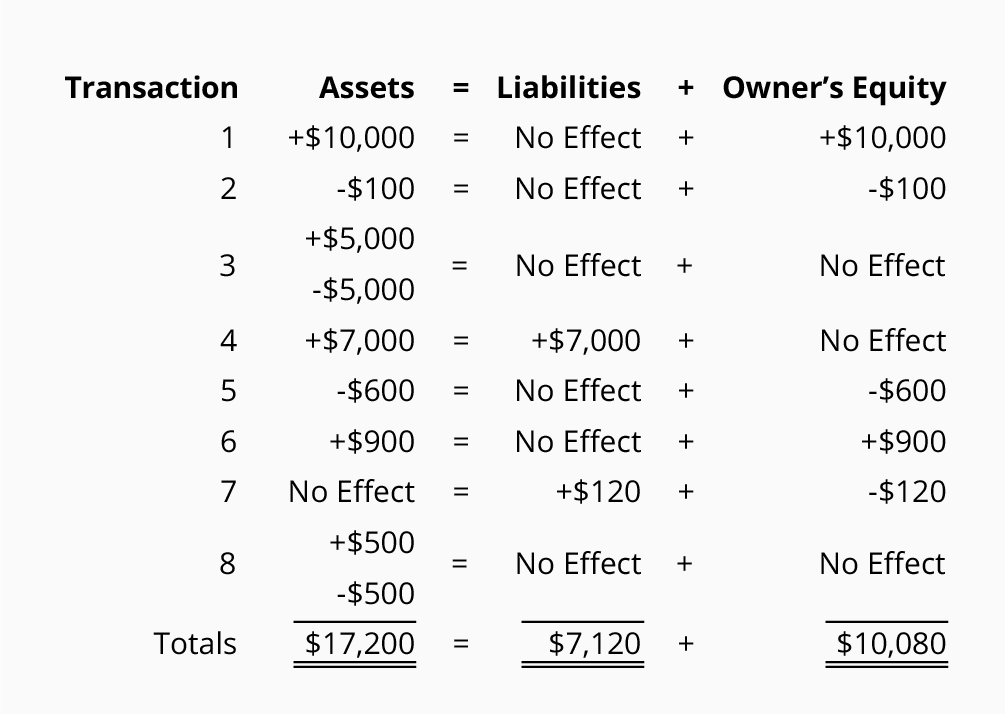

The combined effect of the first eight transactions is shown here:

The totals for the first eight transactions indicate that the company has assets of $17,200. The creditors provided $7,120 and the owner provided $10,080. The accounting equation also indicates that the company's creditors have a claim of $7,120 and the owner has a residual claim of $10,080.

ASC's balance sheet as of midnight December 8, 2019 is:

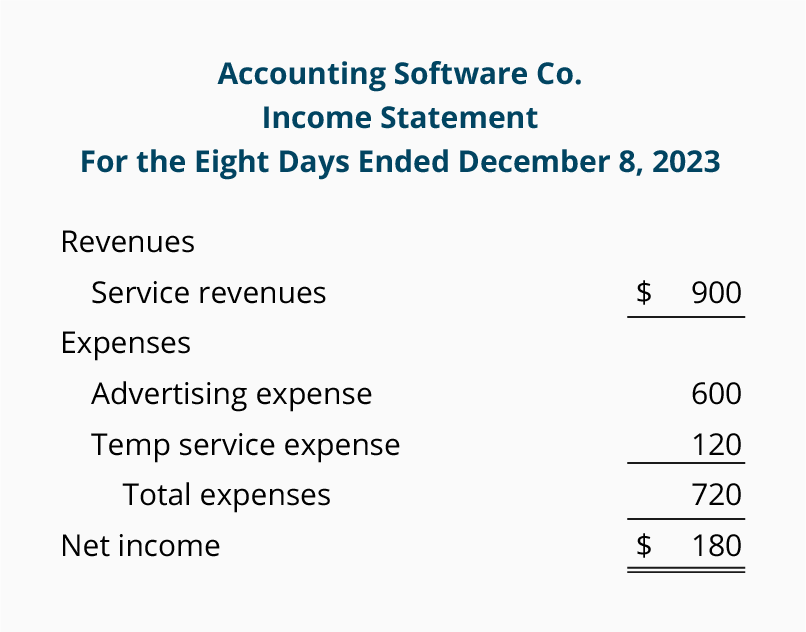

**The income statement (which reports the company's revenues, expenses, gains, and losses during a specified period of time) is a link between balance sheets. It provides the results of operations—an important part of the change in owner's equity.

The income statement for ASC for the eight days ending on December 8 is shown here:

Calculating a Missing Amount within Owner's Equity

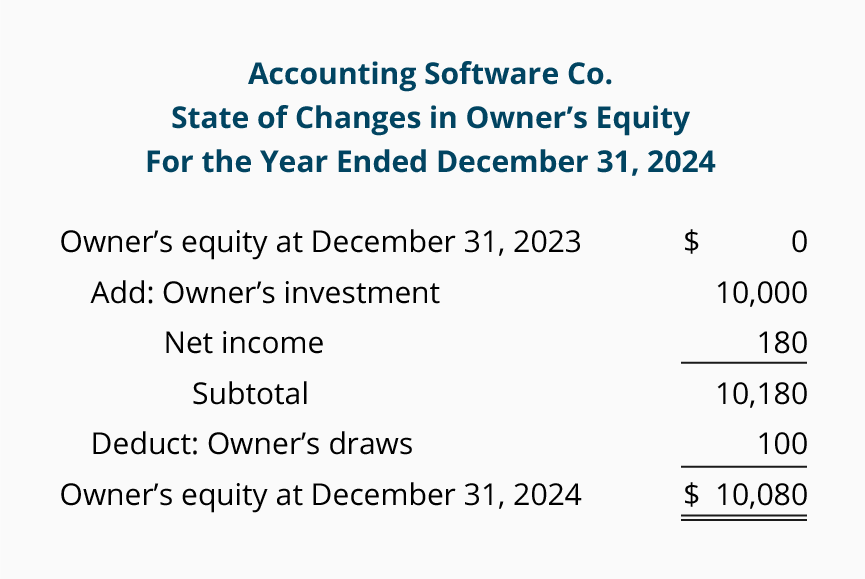

The income statement for the calendar year 2019 will explain a portion of the change in the owner's equity between the balance sheets of December 31, 2018 and December 31, 2019. The other items that account for the change in owner's equity are the owner's investments into the sole proprietorship and the owner's draws (or withdrawals). A recap of these changes is the statement of changes in owner's equity. Here is a statement of changes in owner's equity for the year 2019 assuming that the Accounting Software Co. had only the eight transactions that we covered earlier.

Example of Calculating a Missing Amount

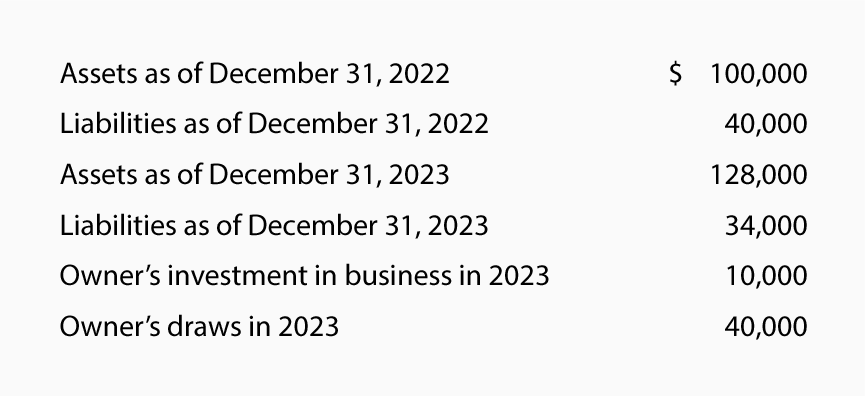

The format of the statement of changes in owner's equity can be used to determine one of these components if it is unknown. For example, if the net income for the year 2019 is unknown, but you know the amount of the draws and the beginning and ending balances of owner's equity, you can calculate the net income. (This might be necessary if a company does not have complete records of its revenues and expenses.) Let's demonstrate this by using the following amounts.

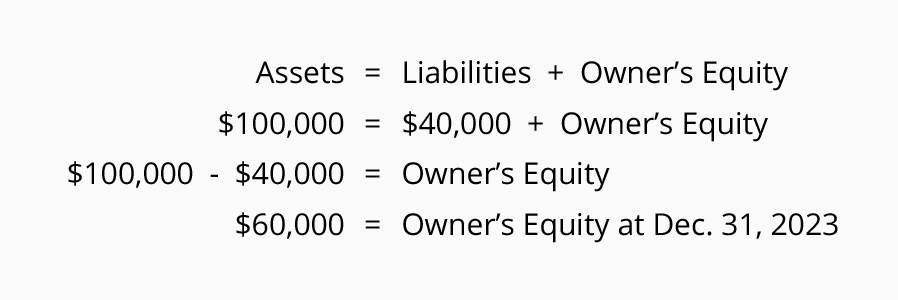

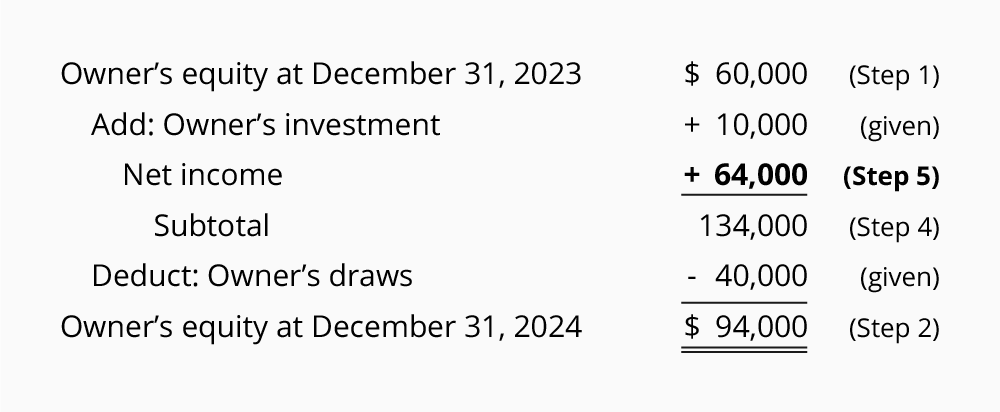

Step 1.

The owner's equity at December 31, 2018 can be computed using the accounting equation:

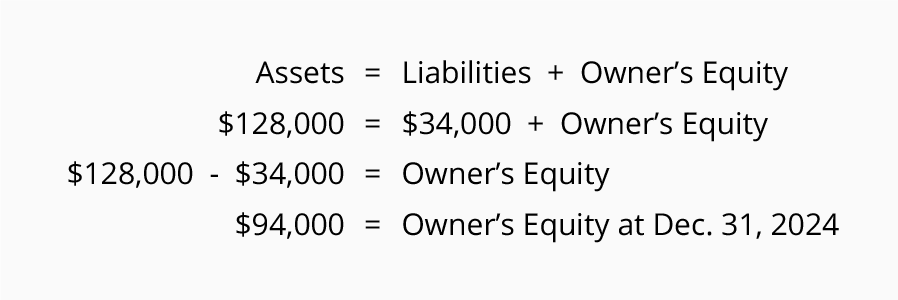

Step 2.

The owner's equity at December 31, 2019 can be computed as well:

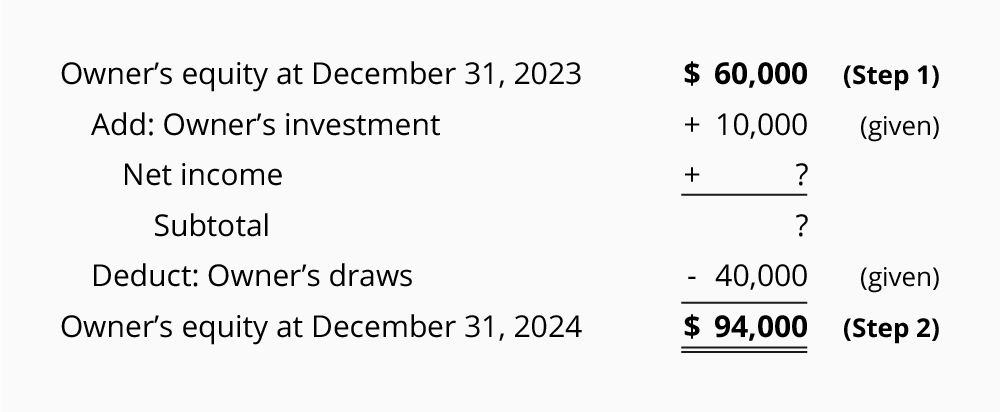

Step 3.

Insert into the statement of changes in owner's equity the information that was given and the amounts calculated in Step 1 and Step 2:

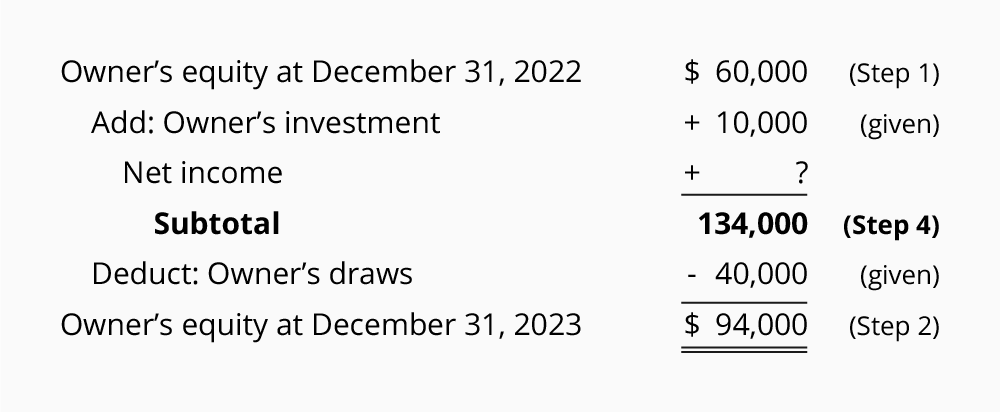

Step 4.

The "Subtotal" can be calculated by adding the last two numbers on the statement: $94,000 + $40,000 = $134,000. After this calculation we have:

Step 5.

Starting at the top of the statement we know that the owner's equity before the start of 2019 was $60,000 and in 2019 the owner invested an additional $10,000. As a result we have $70,000 before considering the amount of Net Income. We also know that after the amount of Net Income is added, the Subtotal has to be $134,000 (the Subtotal calculated in Step 4). The Net Income is the difference between $70,000 and $134,000. Net income must have been $64,000.

Step 6.

Insert the previously missing amount (in this case it is the $64,000 of net income) into the statement of changes in owner's equity and recheck the math:

Since the statement is mathematically correct, we are confident that the net income was $64,000.

FOLLOW US.

Presenting by -Accounting way

for more information -

follow "accounting way" official face book account

subscribe and click the bell icon, to "Accounting tutorials" YouTube channel for practicing knowledge

YouTube channel link mentioned below

https://www.youtube.com/channel/UCpe3Z6l310iM4RcZO1-2mlw

No comments:

Post a Comment