"You will can get notification in to your Gmail ,when we are upload our new article . so you can follow this blog site. you can see "follow button on the top line of the blog page, click it. "

Audit Process

Introduction to the Accounting Equation

From t, every business transaction will have an effect on a company's financial position. The financial position of a company is measured by the following items:

- Assets (what it owns)

- Liabilities (what it owes to others)

- Owner's Equity (the difference between assets and liabilities)

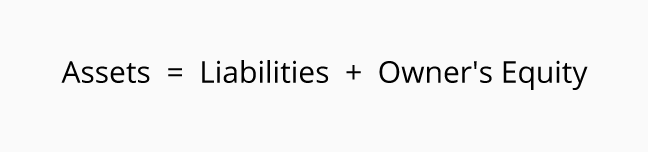

The accounting equation (or basic accounting equation) offers us a simple way to understand how these three amounts relate to each other. The accounting equation for a sole proprietorship is:

The accounting equation for a corporation is:

Assets are a company's resources—things the company owns. Examples of assets include cash, accounts receivable, inventory, prepaid insurance, investments, land, buildings, equipment, and goodwill. From the accounting equation, we see that the amount of assets must equal the combined amount of liabilities plus owner's (or stockholders') equity.

Liabilities are a company's obligations—amounts the company owes. Examples of liabilities include notes or loans payable, accounts payable, salaries and wages payable, interest payable, and income taxes payable (if the company is a regular corporation). Liabilities can be viewed in two ways:

(1) as claims by creditors against the company's assets, and

(2) a source—along with owner or stockholder equity—of the company's assets.

Owner's equity or stockholders' equity is the amount left over after liabilities are deducted from assets:

Assets - Liabilities = Owner's (or Stockholders') Equity.

Owner's or stockholders' equity also reports the amounts invested into the company by the owners plus the cumulative net income of the company that has not been withdrawn or distributed to the owners.

If a company keeps accurate records, the accounting equation will always be "in balance," meaning the left side should always equal the right side. The balance is maintained because every business transaction affects at least two of a company's accounts. For example, when a company borrows money from a bank, the company's assets will increase and its liabilities will increase by the same amount. When a company purchases inventory for cash, one asset will increase and one asset will decrease. Because there are two or more accounts affected by every transaction, the accounting system is referred to as double-entry accounting.

A company keeps track of all of its transactions by recording them in accounts in the company's general ledger. Each account in the general ledger is designated as to its type: asset, liability, owner's equity, revenue, expense, gain, or loss account.

Balance Sheet and Income Statement

The balance sheet is also known as the statement of financial position and it reflects the accounting equation. The balance sheet reports a company's assets, liabilities, and owner's (or stockholders') equity at a specific point in time. Like the accounting equation, it shows that a company's total amount of assets equals the total amount of liabilities plus owner's (or stockholders') equity.

The income statement is the financial statement that reports a company's revenues and expenses and the resulting net income. While the balance sheet is concerned with one point in time, the income statement covers a time interval or period of time. The income statement will explain part of the change in the owner's or stockholders' equity during the time interval between two balance sheets.

Examples

In our examples in the following pages of this topic, we show how a given transaction affects the accounting equation. We also show how the same transaction affects specific accounts by providing the journal entry that is used to record the transaction in the company's general ledger.

Accounting Equation for a Sole Proprietorship: Transactions 1-2

We present nine transactions to illustrate how a company's accounting equation stays in balance.

When a company records a business transaction, it is not entered into an accounting equation, per se. Rather, transactions are recorded into specific accounts contained in the company's general ledger. Each account is designated as an asset, liability, owner's equity, revenue, expense, gain, or loss account. The general ledger accounts are then used to prepare the balance sheets and income statements throughout the accounting periods.

In the examples that follow, we will use the following accounts:

- Cash

- Accounts Receivable

- Equipment

- Notes Payable

- Accounts Payable

- J. Ott, Capital

- J. Ott, Drawing

- Service Revenues

- Advertising Expense

- Temp Service Expense

(To view a more complete listing of accounts for recording transactions, see the Explanation of Chart of Accounts.)

Sole Proprietorship Transaction #1.

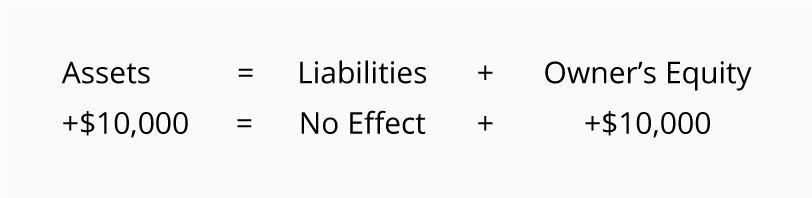

Let's assume that J. Ott forms a sole proprietorship called Accounting Software Co. (ASC). On December 1, 2019, J. Ott invests personal funds of $10,000 to start ASC. The effect of this transaction on ASC's accounting equation is:

As you can see, ASC's assets increase by $10,000 and so does ASC's owner's equity. As a result, the accounting equation will be in balance.

You can interpret the amounts in the accounting equation to mean that ASC has assets of $10,000 and the source of those assets was the owner, J. Ott. Alternatively, you can view the accounting equation to mean that ASC has assets of $10,000 and there are no claims by creditors (liabilities) against the assets. As a result, the owner has a claim for the remainder or residual of $10,000.

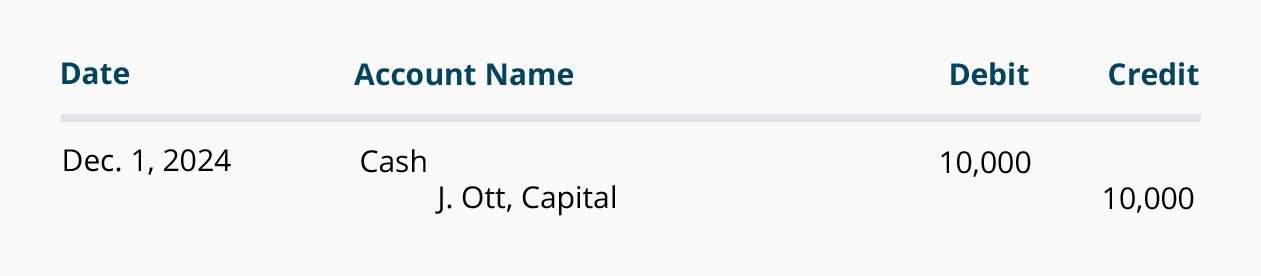

This transaction is recorded in the asset account Cash and the owner's equity account J. Ott, Capital. The general journal entry to record the transactions in these accounts is:

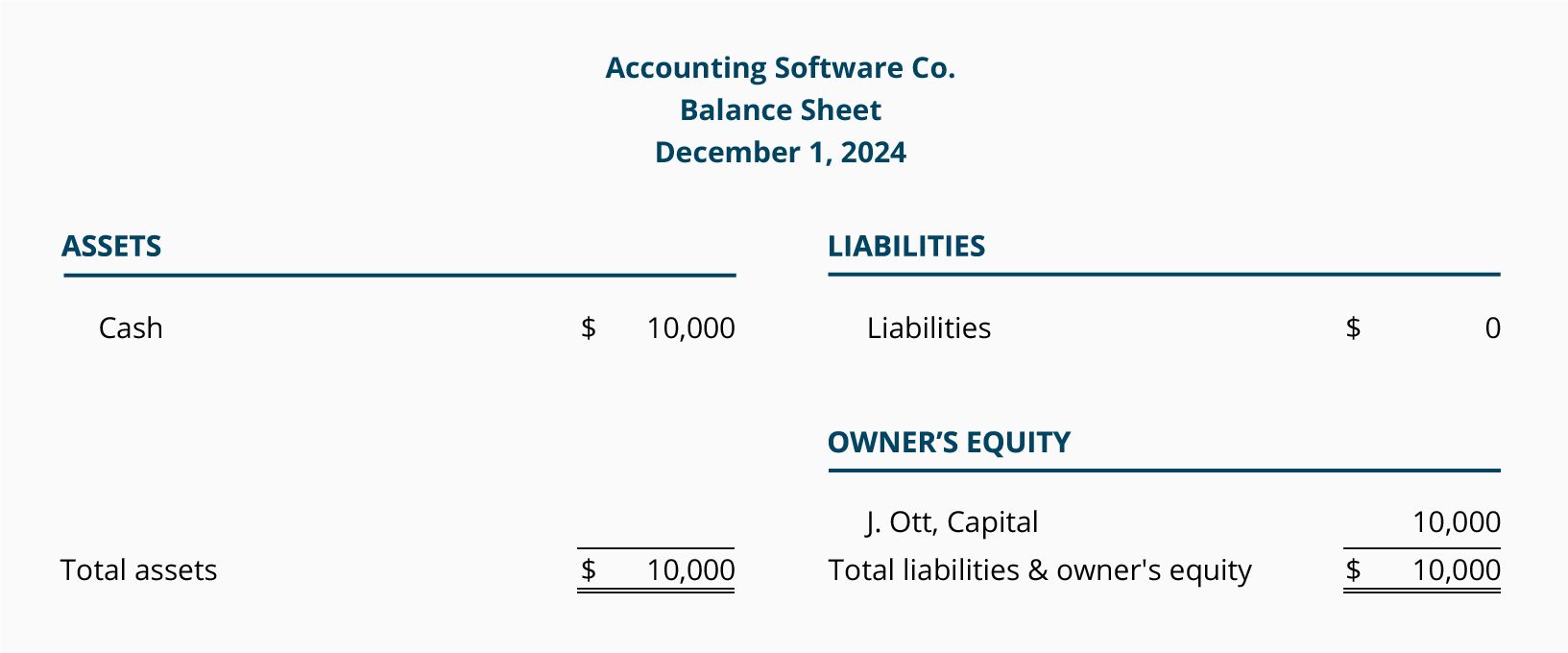

After the journal entry is recorded in the accounts, a balance sheet can be prepared to show ASC's financial position at the end of December 1, 2019:

The purpose of an income statement is to report revenues and expenses. Since ASC has not yet earned any revenues nor incurred any expenses, there are no transactions to be reported on an income statement.

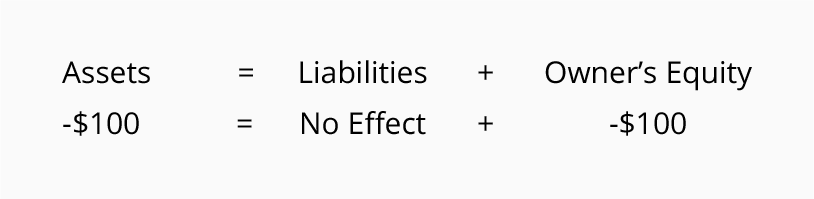

Sole Proprietorship Transaction #2.

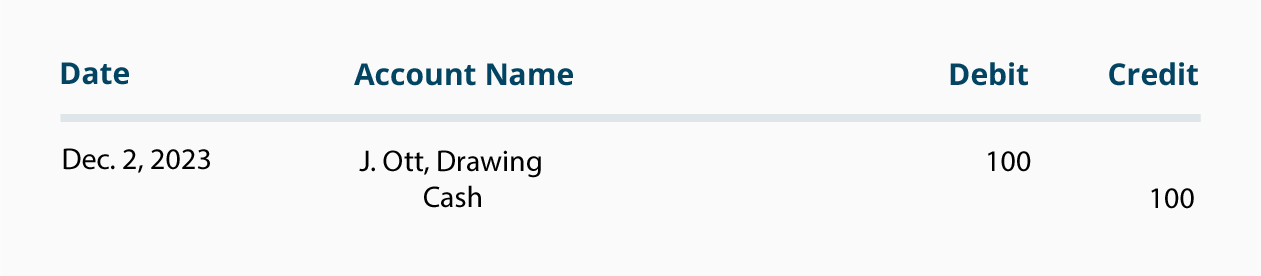

On December 2, 2019 J. Ott withdraws $100 of cash from the business for his personal use. The effect of this transaction on ASC's accounting equation is:

The accounting equation remains in balance since ASC's assets have been reduced by $100 and so has the owner's equity.

This transaction is recorded in the asset account Cash and the owner's equity account J. Ott, Drawing. The general journal entry to record the transactions in these accounts is:

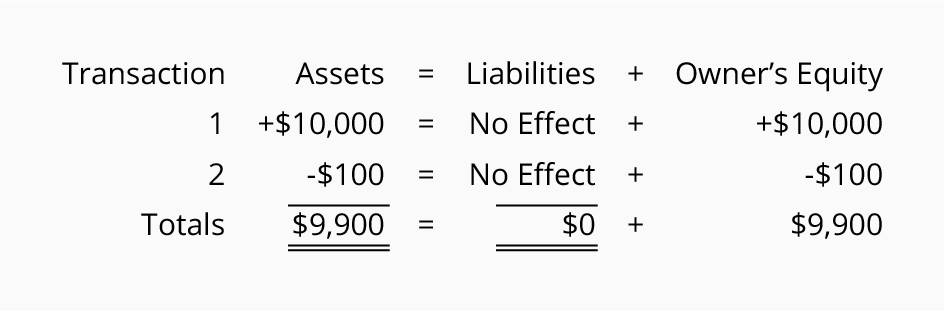

Since the transactions of December 1 and 2 were each in balance, the sum of both transactions should also be in balance:

The totals indicate that ASC has assets of $9,900 and the source of those assets is the owner of the company. You can also conclude that the company has assets or resources of $9,900 and the only claim against those resources is the owner's claim.

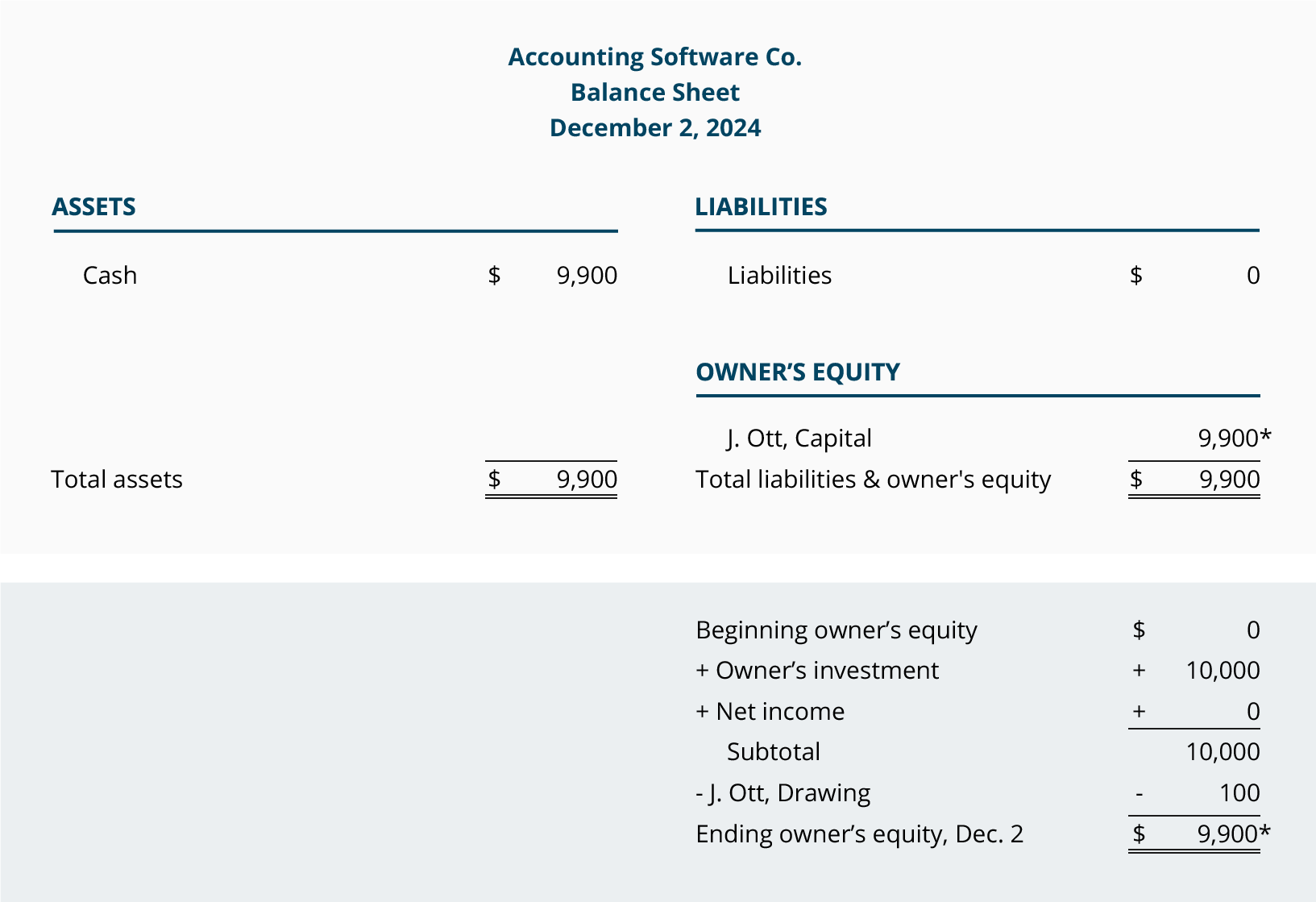

The December 2 balance sheet will communicate the company's financial position as of midnight on December 2:

Withdrawals of company assets by the owner for the owner's personal use are known as "draws." Since draws are not expenses, the transaction is not reported on the company's income statement.

Accounting Equation for a Sole Proprietorship: Transactions 3-4

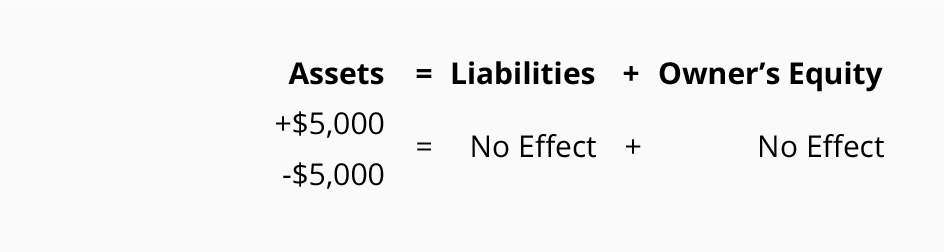

Sole Proprietorship Transaction #3.

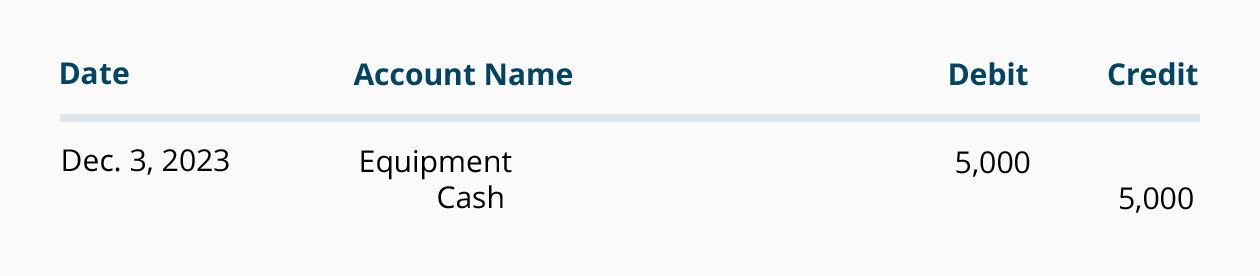

On December 3, 2019 Accounting Software Co. spends $5,000 of cash to purchase computer equipment for use in the business. The effect of this transaction on the accounting equation is:

The accounting equation reflects that one asset increases and another asset decreases. Since the amount of the increase is the same as the amount of the decrease, the accounting equation remains in balance.

This transaction is recorded in the asset accounts Equipment and Cash. Equipment increases by $5,000, and Cash decreases by $5,000. The general journal entry to record the transactions in these accounts is:

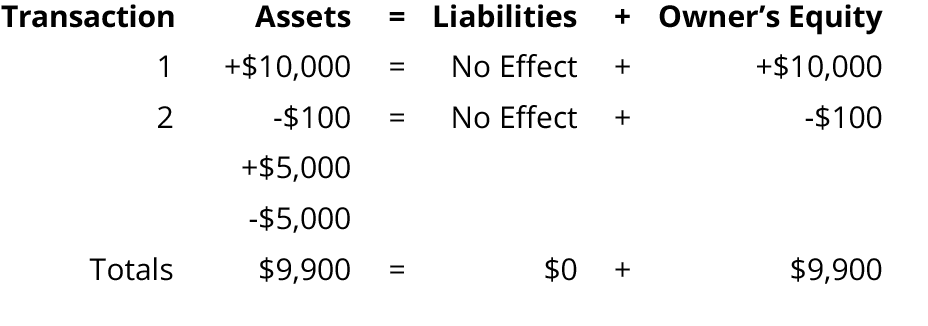

The combined effect of the first three transactions is shown here:

The totals tell us that the company has assets of $9,900 and the source of those assets is the owner of the company. It also tells us that the company has assets of $9,900 and the only claim against those assets is the owner's claim.

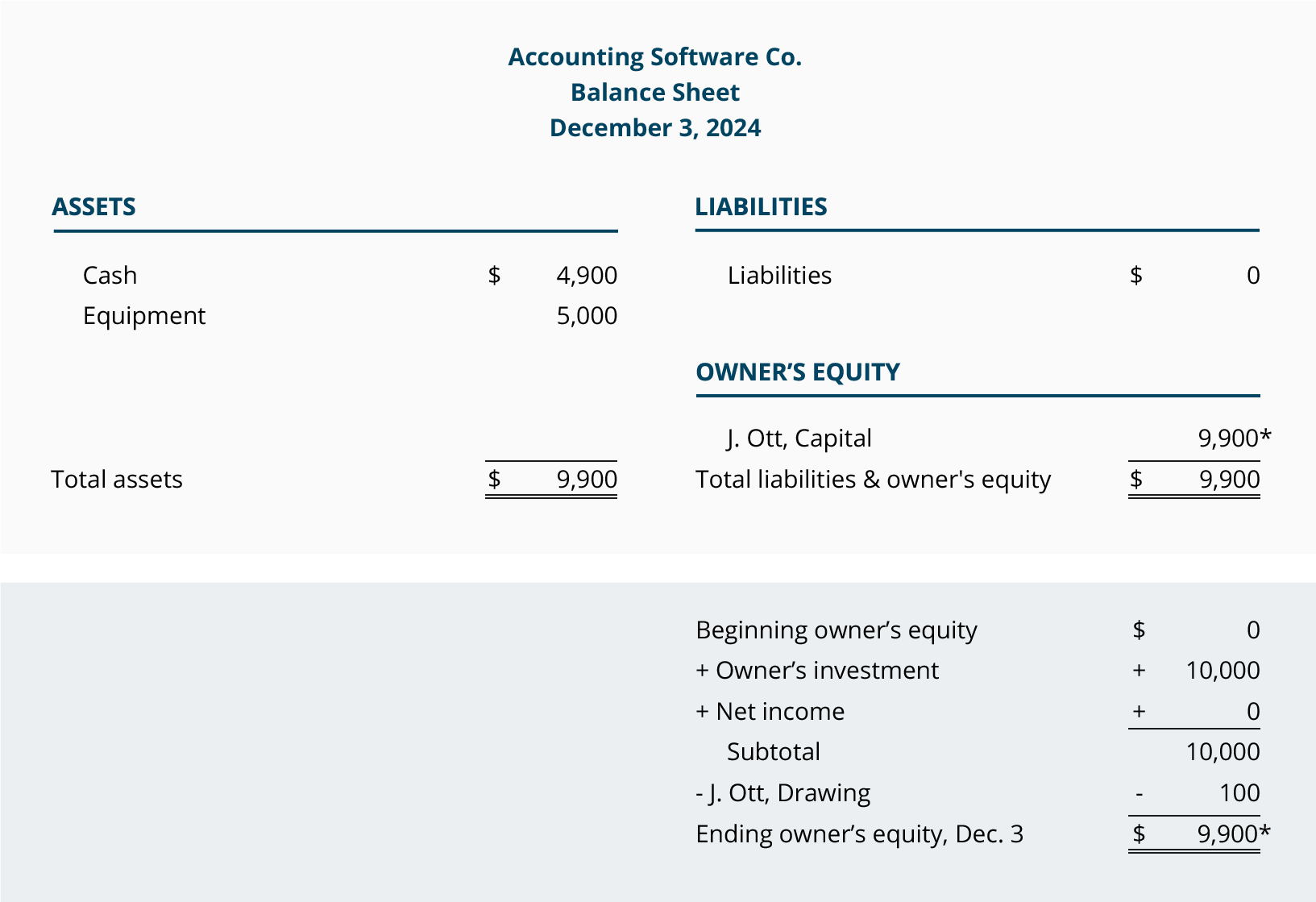

The balance sheet dated December 3, 2019 will reflect the financial position as of midnight on December 3:

The purchase of equipment is not an immediate expense. It will become part of depreciation expense only after it is placed into service. We will assume that as of December 3 the equipment has not been placed into service, therefore, no expense will appear on an income statement for the period of December 1 through December 3.

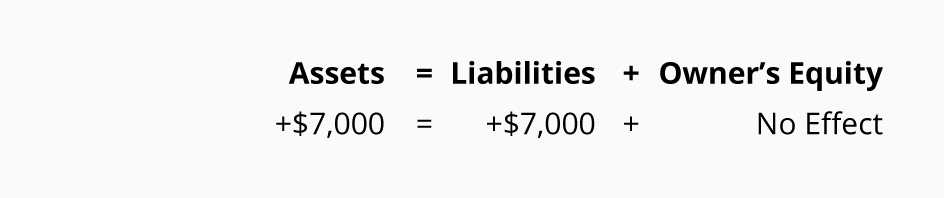

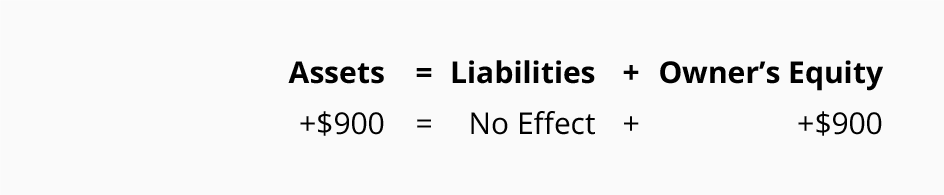

Sole Proprietorship Transaction #4.

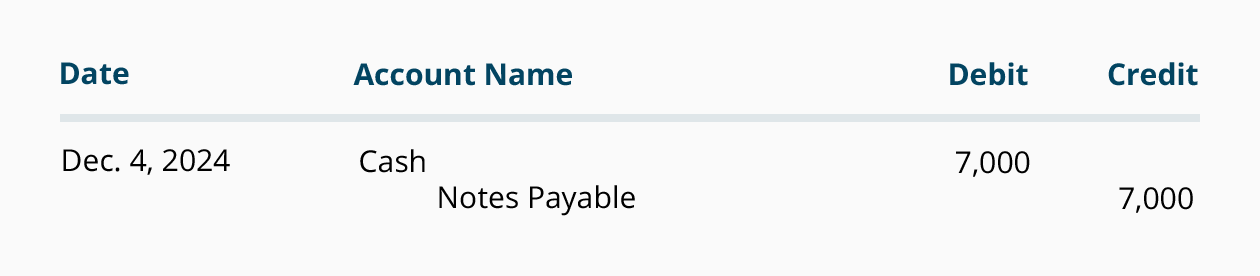

On December 4, 2019 ASC obtains $7,000 by borrowing money from its bank. The effect of this transaction on the accounting equation is:

As you can see, ASC's assets increase and ASC's liabilities increase by $7,000.

This transaction is recorded in the asset account Cash and the liability account Notes Payable as shown in this accounting entry:

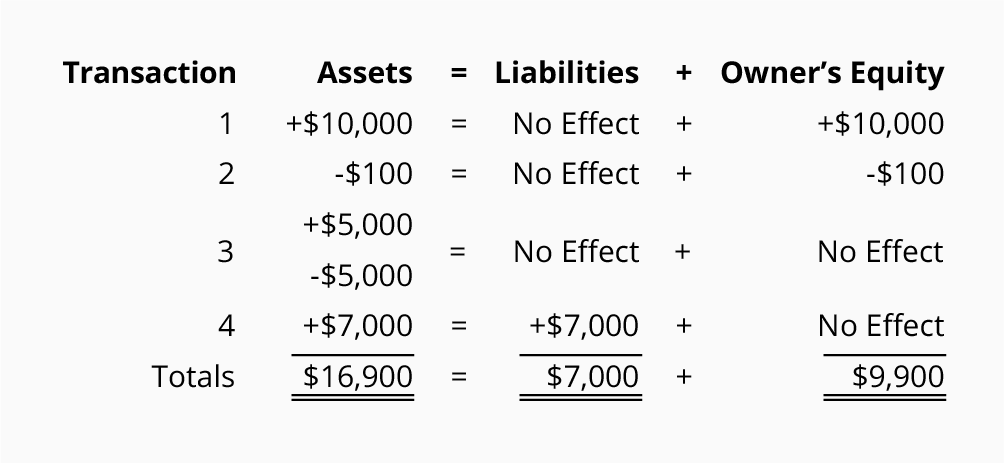

The combined effect on the accounting equation from the first four transactions is available here:

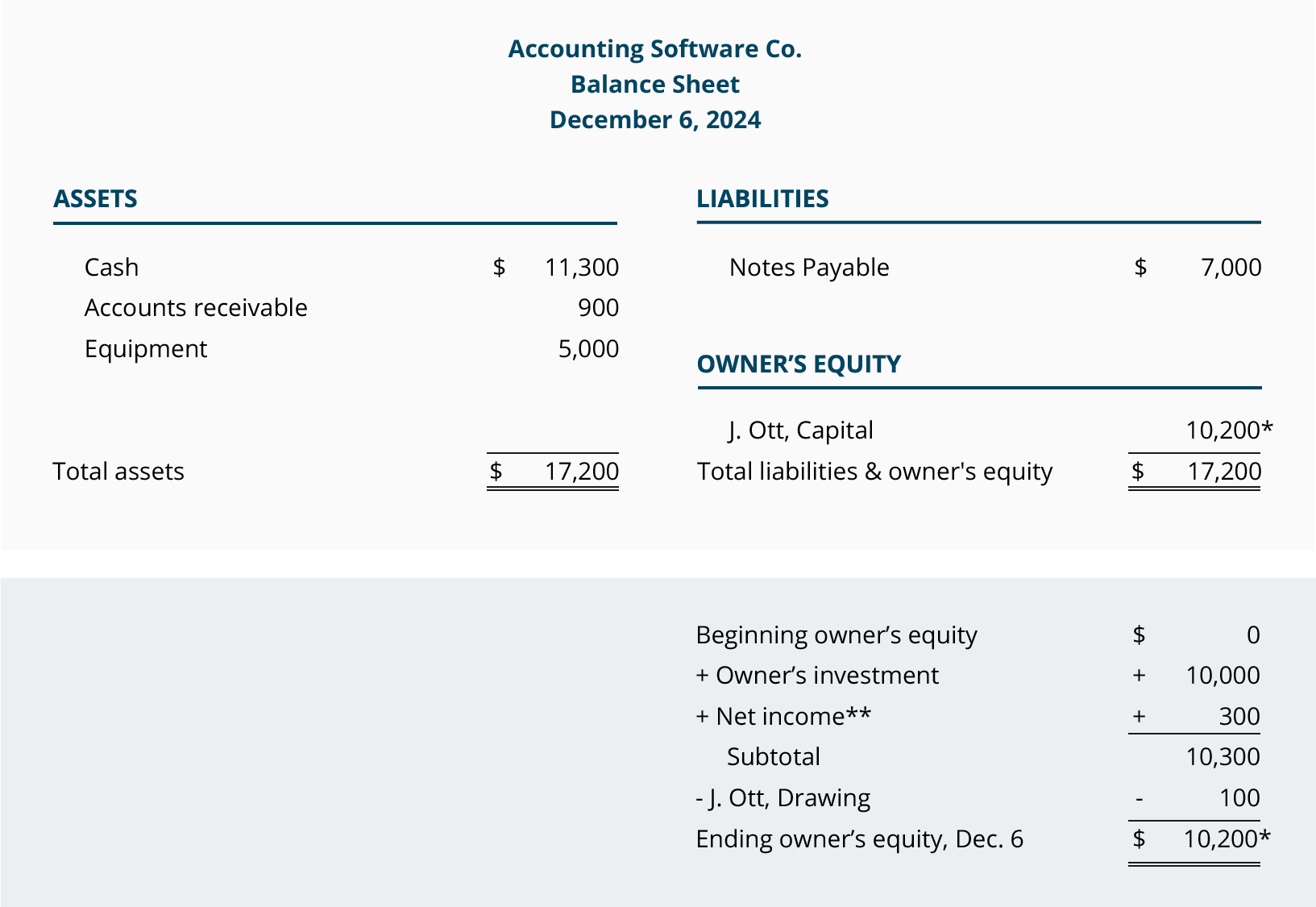

The totals indicate that the transactions through December 4 result in assets of $16,900. There are two sources for those assets—the creditors provided $7,000 of assets, and the owner of the company provided $9,900. You can also interpret the accounting equation to say that the company has assets of $16,900 and the lenders have a claim of $7,000 and the owner has a claim for the remainder.

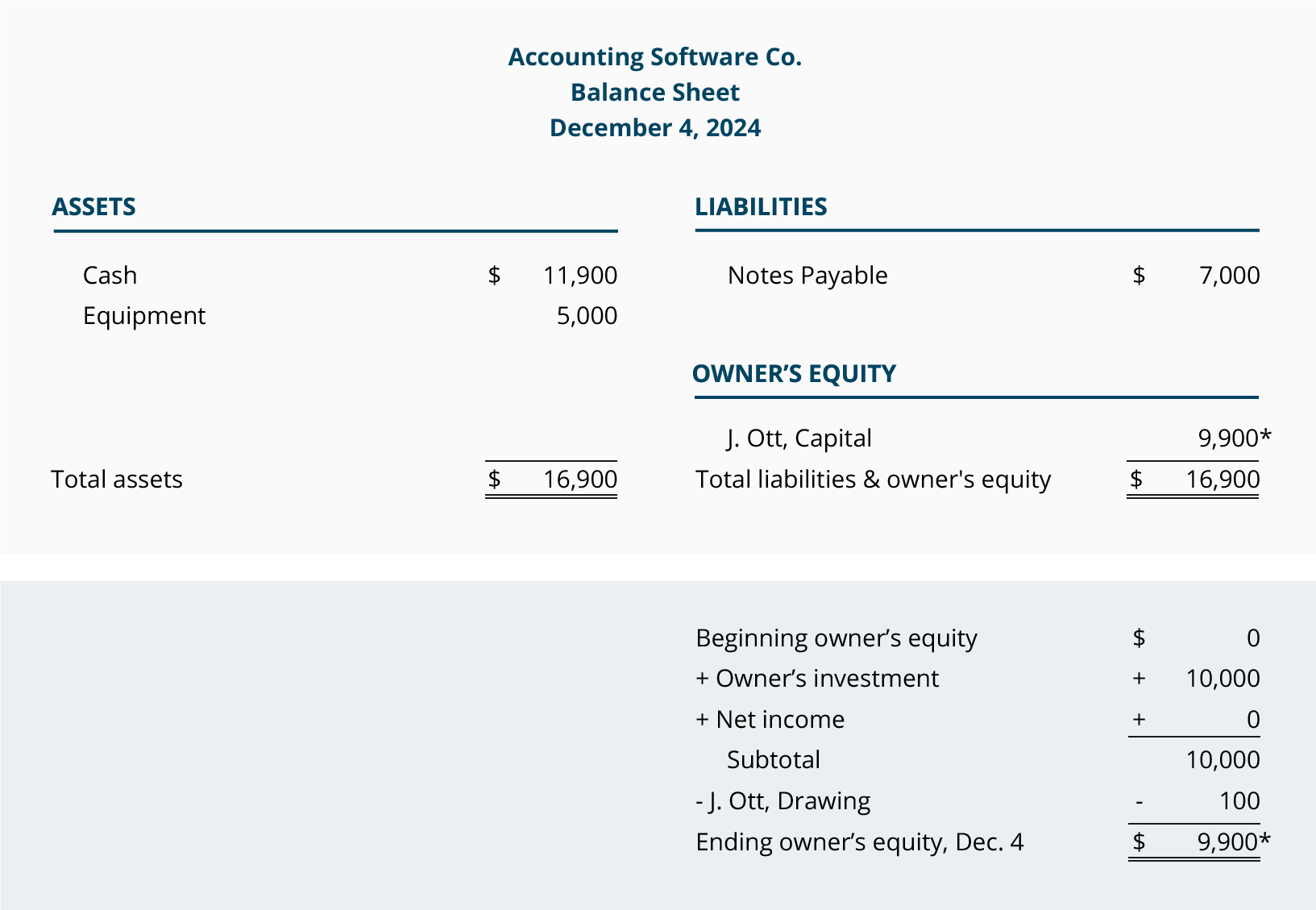

The balance sheet dated December 4 will report ASC's financial position as of that date:

The proceeds of the bank loan are not considered to be revenue since ASC did not earn the money by providing services, investing, etc. As a result, there is no income statement effect from this transaction.

Accounting Equation for a Sole Proprietorship: Transactions 5-6

Sole Proprietorship Transaction #5.

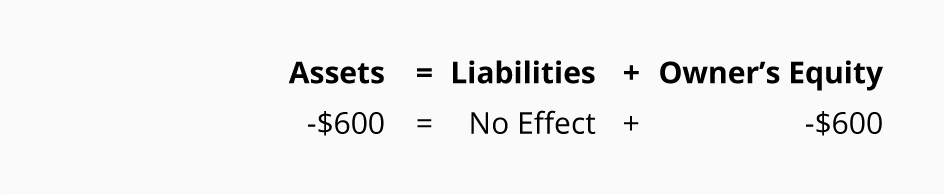

On December 5, 2019 Accounting Software Co. pays $600 for ads that were run in recent days. The effect of this advertising transaction on the accounting equation is:

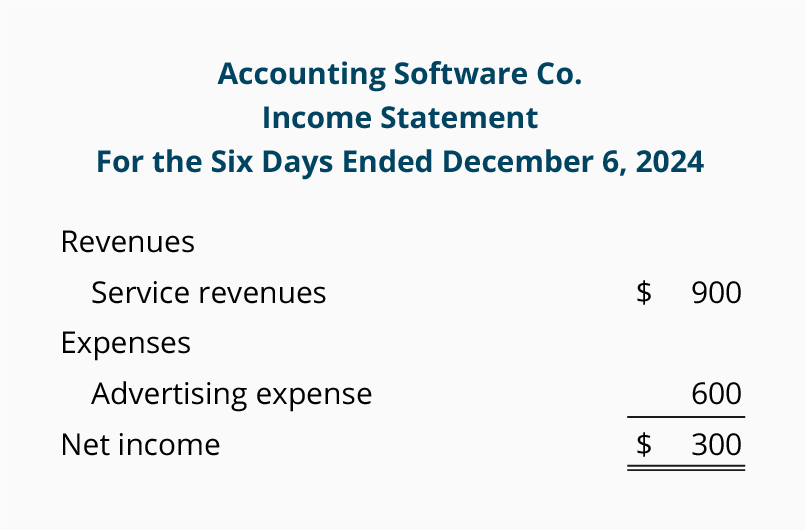

Since ASC is paying $600, its assets decrease. The second effect is a $600 decrease in owner's equity, because the transaction involves an expense. (An expense is a cost that is used up or its future economic value cannot be measured.)

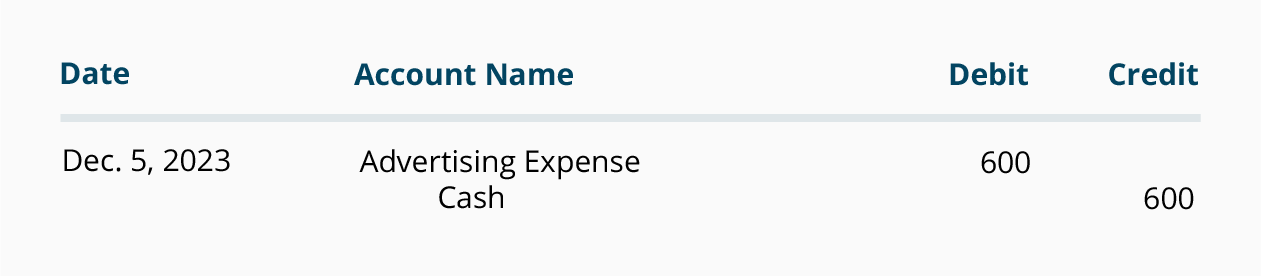

Although owner's equity is decreased by an expense, the transaction is not recorded directly into the owner's capital account at this time. Instead, the amount is initially recorded in the expense account Advertising Expense and in the asset account Cash.

The general journal entry to record the transaction is:

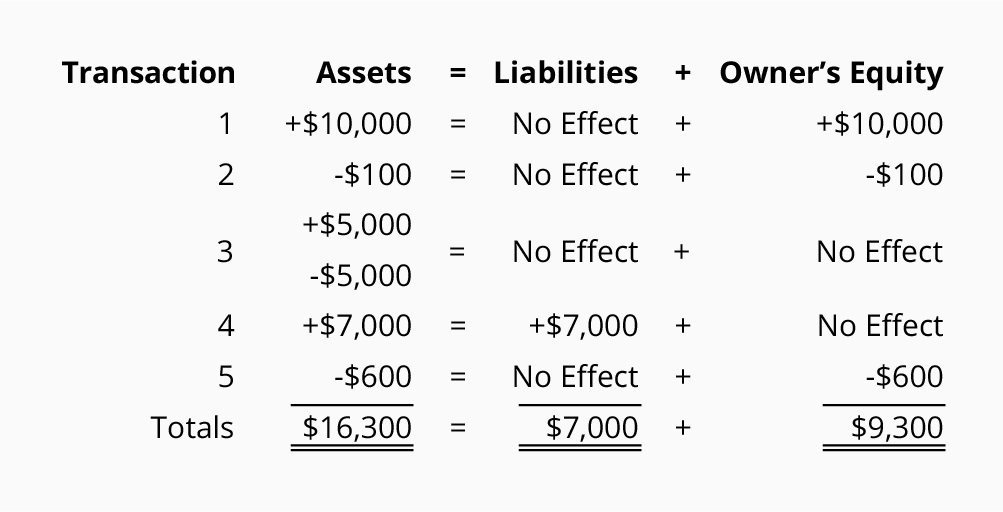

The combined effect of the first five transactions is available here:

The totals now indicate that Accounting Software Co. has assets of $16,300. The creditors provided $7,000 and the owner of the company provided $9,300. Viewed another way, the company has assets of $16,300 with the creditors having a claim of $7,000 and the owner having a residual claim of $9,300.

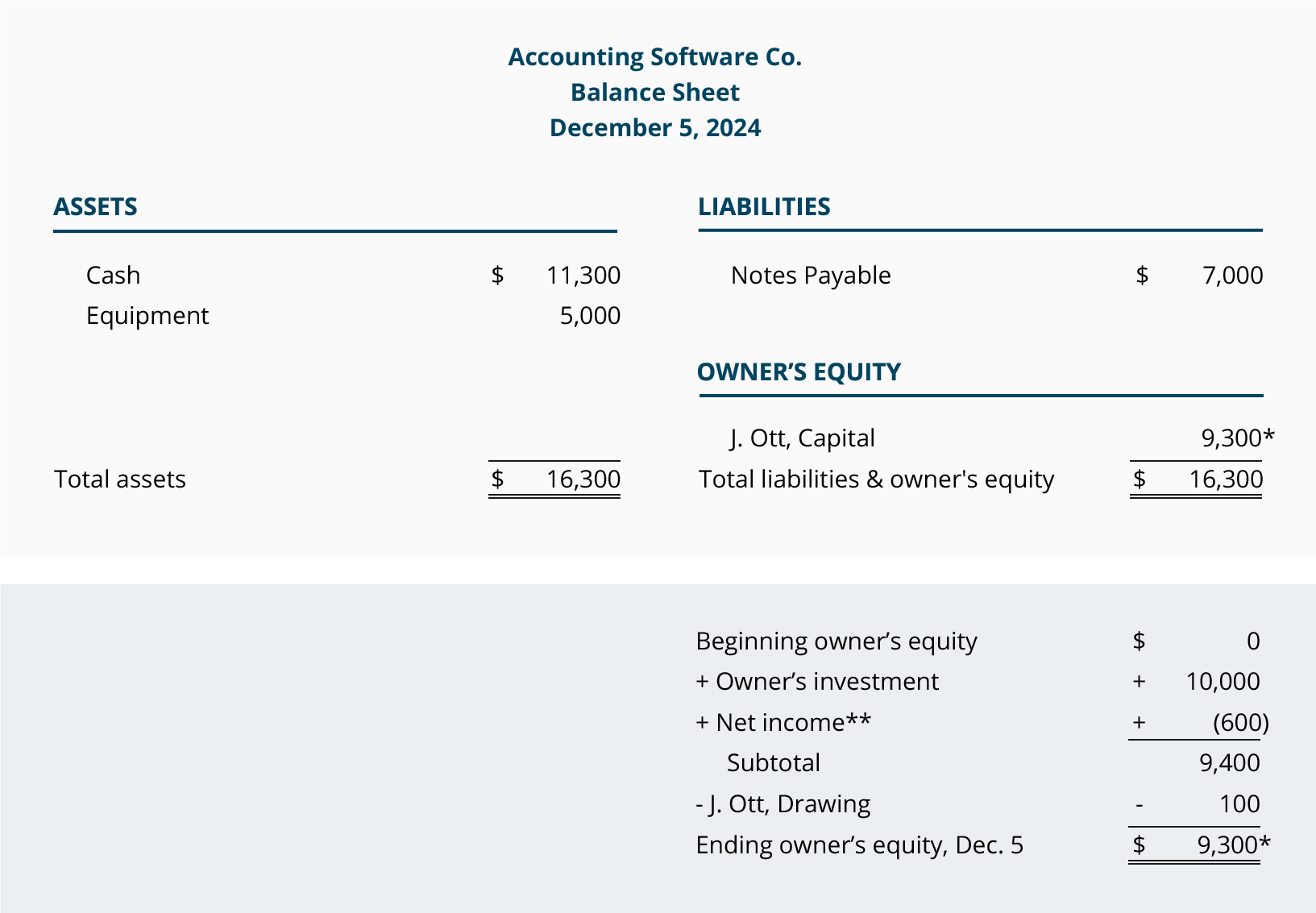

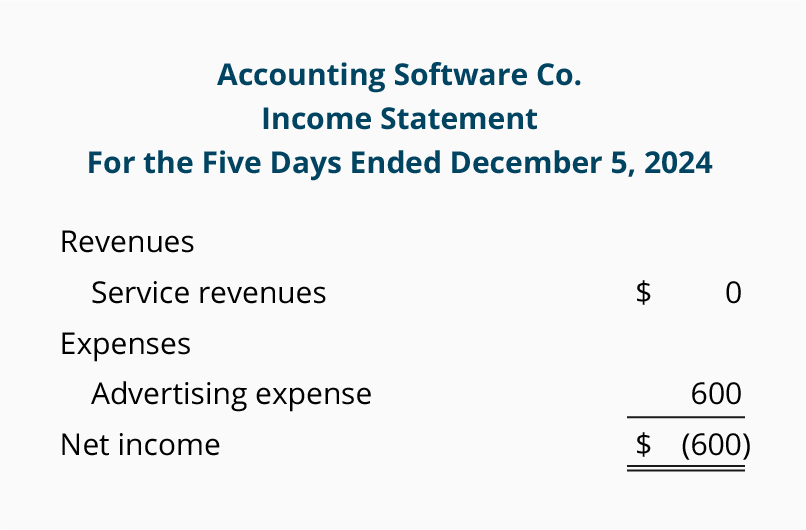

The balance sheet as of the end of December 5, 2019 is:

**The income statement (which reports the company's revenues, expenses, gains, and losses during a specified time interval) is a link between balance sheets. It provides the results of operations—an important part of the change in owner's equity.

Since this transaction involves an expense, it will involve ASC's income statement. The company's income statement for the first five days of December is:

Sole Proprietorship Transaction #6.

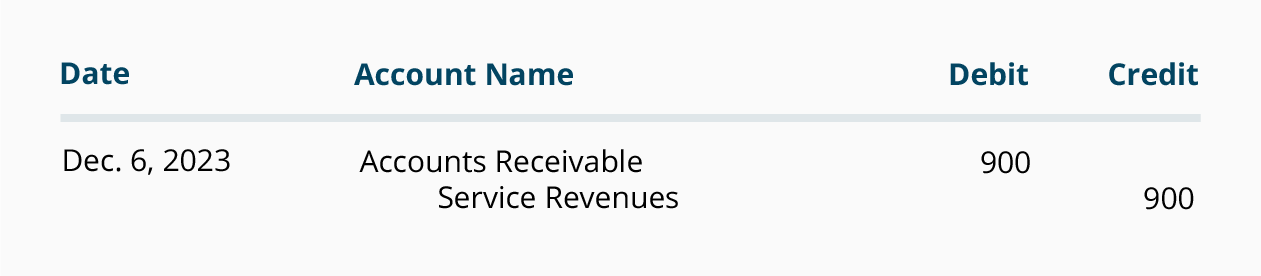

On December 6, 2019 ASC performs consulting services for its clients. The clients are billed for the agreed upon amount of $900. The amounts are due in 30 days. The effect on the accounting equation is:

Since ASC has performed the services, it has earned revenues and it has the right to receive $900 from the clients. This right (known as an account receivable) causes assets to increase. The earning of revenues causes owner's equity to increase.

Although revenues cause owner's equity to increase, the revenue transaction is not recorded into the owner's capital account at this time. Rather, the amount earned is recorded in the revenue account Service Revenues. This will allow the company to report the revenues on its income statement at any time. (After the year ends, the amount in the revenue account will be transferred to the owner's capital account.)

The general journal entry to record the transaction is:

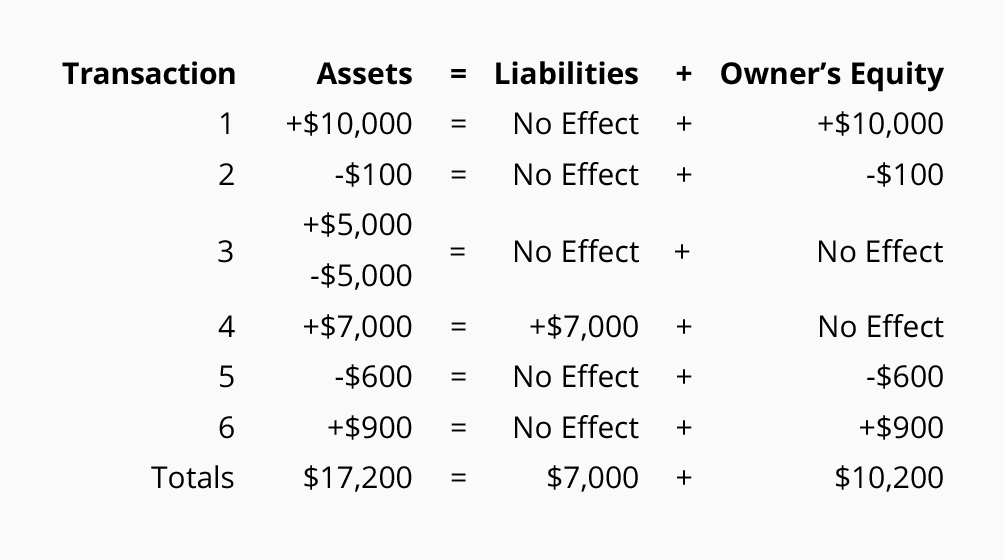

The combined effect of the first six transactions can be viewed here:

The totals tell us that at the end of December 6, the company has assets of $17,200. It also shows the sources of the assets: creditors providing $7,000 and the owner of the company providing $10,200. The totals also reveal that the company has assets of $17,200 and the creditors have a claim of $7,000 and the owner has a claim for the remaining $10,200.

Below is the balance sheet as of midnight on December 6:

**The income statement (which reports the company's revenues, expenses, gains, and losses during a specified time interval) is a link between balance sheets. It provides the results of operations—an important part of the change in owner's equity.

The Income Statement for Accounting Software Co. for the period of December 1 through December 6 is:

Thank you. .

(Comment your suggestions)

FOLLOW US.

Presenting by -Accounting way

for more information -

follow "accounting way" official face book account

subscribe and click the bell icon, to "Accounting tutorials" YouTube channel for practicing knowledge

YouTube channel link mentioned be below

https://www.youtube.com/channel/UCpe3Z6l310iM4RcZO1-2mlw

No comments:

Post a Comment